If you have an FHA loan and need access to better terms or home equity, you may be deciding between:

Refinancing your FHA loan, or Opening a HELOC (Home Equity Line of Credit) At first glance, both options can improve flexibility.

In real-world scenarios reviewed by our lending team, homeowners often choose the wrong tool — not because of rate, but because they misunderstand structure and long-term cost.

Let’s break it down clearly.

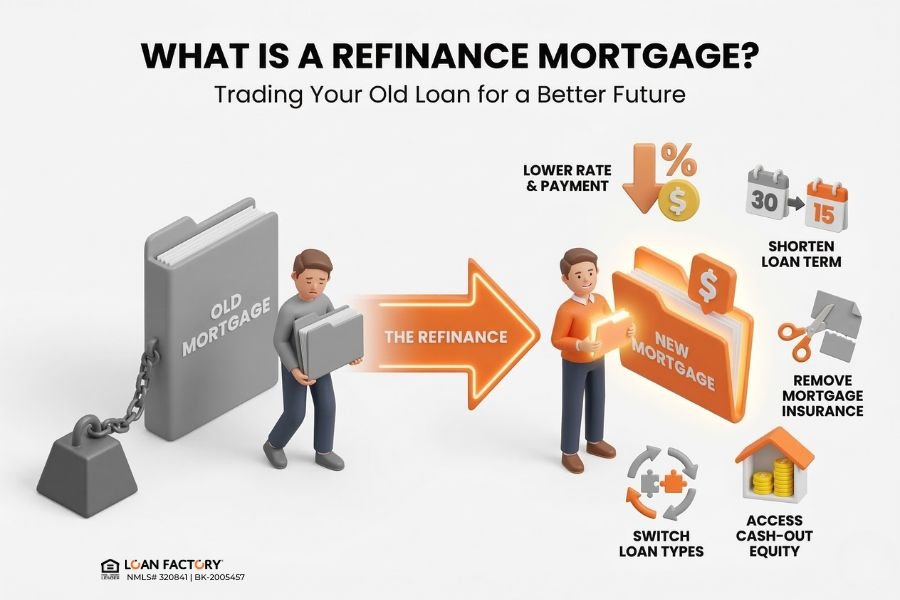

What Is an FHA Refinance? An FHA refinance replaces your current mortgage with a new loan.

Options may include:

Homeowners typically refinance to:

Lower their interest rate (when market conditions allow) Remove FHA mortgage insurance (if switching to conventional) Adjust loan term Access equity through cash-out If you’re unsure how FHA mortgage insurance works, review our full guide on FHA mortgage insurance explained.

→ Read more: Can You Refinance FHA With Less Than 20% Equity?

What Is a HELOC? A HELOC (Home Equity Line of Credit) is a second lien loan.

It allows you to:

Borrow against available equity Access funds as needed (like a credit line) Keep your existing first mortgage unchanged Key features:

Variable interest rate (most common) Interest-only payment options during draw period Flexible borrowing A HELOC does not replace your FHA loan.

It sits behind it.

Feature

FHA Refinance

HELOC

Replaces Existing Loan Yes No Removes FHA MIP Possibly (if switching to conventional) No Access Equity Yes (cash-out option) Yes Affects First Mortgage Rate Yes No Creates Second Payment No Yes Rate Type Fixed or adjustable Usually variable Long-Term Restructuring Yes Limited

The better option depends on your goal.

When FHA Refinance May Make More Sense Refinancing may be stronger if you want to:

Remove FHA Mortgage Insurance If you have enough equity, switching to conventional may eliminate MIP entirely.

See our breakdown of how much equity you need to remove FHA MIP.

→ Read more: FHA Mortgage Insurance Explained: How MIP Works and When It Ends

Restructure Your Entire Loan Refinancing allows you to:

Change term (30-year to 15-year, etc.) Reset amortization Consolidate debt into one payment Lock a Fixed Rate If stability matters more than flexibility, refinancing may offer predictable long-term structure.

When a HELOC May Make More Sense A HELOC may be better if:

You Want to Keep Your Low FHA Rate If your current FHA interest rate is significantly lower than today’s market rates, replacing it might not be ideal.

A HELOC allows you to keep your first mortgage intact.

You Need Flexible Access to Funds HELOCs are useful for:

Renovations Business use Emergency reserves Staggered spending You Don’t Want to Reset Your Loan Term Refinancing resets amortization.

The Mortgage Insurance Factor One of the biggest decision drivers is FHA mortgage insurance.

If your FHA loan requires lifetime MIP (common with less than 10% down), a HELOC will not eliminate it.

Only refinancing into a conventional loan may remove that cost.

If you're unsure when refinancing makes sense, review our guide on when you should refinance an FHA loan.

Risk & Payment Structure Differences FHA Refinance One monthly payment Long-term commitment Structured amortization HELOC Two payments (mortgage + line of credit) Variable interest exposure Payment may increase over time In several cases reviewed internally, borrowers underestimated the long-term cost of variable HELOC rates.

Structure matters more than short-term flexibility.

Cost Comparison Considerations Before choosing, evaluate:

Your current FHA interest rate Remaining loan balance Available equity Closing costs HELOC rate structure Long-term plans If you’re unsure how to compare costs, see our guide on how to calculate your refinance break-even point.

Sometimes the smartest move is strategic patience

So… Which Makes More Sense? Choose FHA Refinance if:

You want to eliminate FHA mortgage insurance You want one consolidated payment You plan to stay long term Your credit and equity support conventional pricing Choose HELOC if:

You want flexible access to equity You have a strong existing FHA rate You only need short-term liquidity You don’t want to reset your loan The right answer depends on your financial goals — not just current rates.

Why Homeowners Compare FHA Refinance vs HELOC with Loan Factory This decision isn’t about choosing a product.

It’s about structuring your equity wisely.

Why Homeowners Choose Loan Factory:

Best Price Guarantee – If Loan Factory can’t beat a competitor’s official offer, you get $2,000 (Terms & Conditions apply)Zero application or junk fees Transparent side-by-side comparison of 240+ wholesale lenders Access to both refinance and home equity lending options AI-powered MOSO platform for real-time scenario comparisons Trusted guidance led by Thuan Nguyen, #1 Loan Officer in the U.S. We don’t push one path.

We compare both — so you can see which structure aligns with your long-term goals.

Ready to Compare FHA Refinance and HELOC Options? Apply online: https://www.LoanFactory.com/apply https://www.LoanFactory.com/quote www.loanfactory.com/mortgage-rate-alert

Based on real-world jumbo loan scenarios reviewed by Loan Factory’s lending team across multiple high-cost markets.

This content is for informational purposes only and not a commitment to lend. Loan options, rates, and terms depend on credit, income, property value, underwriting, and investor guidelines.

FAQ: FHA Refinance vs HELOC