Refinancing a mortgage is one of the most common financial strategies U.S. homeowners use to adjust their loan terms, reduce long-term costs, or access home equity.

However, refinancing is not simply about getting a lower interest rate. Timing, equity position, credit profile, and lender structure all influence whether refinancing actually improves your financial situation.

In today’s rate environment, many homeowners are asking the same question:

Does refinancing still make sense?

This guide explains how refinance mortgages work, when refinancing may make sense, and how experienced lending teams evaluate refinance scenarios in the current market.

A refinance mortgage replaces your existing home loan with a new one.

The new loan pays off your current mortgage balance, and you begin making payments under a new loan structure.

Homeowners typically refinance to:

Potentially reduce their interest rate Lower their monthly payment Shorten the loan term (for example, switching from a 30-year loan to a 15-year loan) Remove mortgage insurance such as PMI or FHA MIP Access equity through a cash-out refinance Switch loan types (for example FHA to Conventional) Refinancing can change both the cost structure and long-term trajectory of a mortgage, which is why experienced loan advisors often evaluate the break-even timeline and total cost before recommending a refinance.

Different refinance structures serve different financial goals.

Refinance Type

Primary Purpose

Common Scenario

Rate-and-Term Refinance Adjust interest rate or loan term Lower payment or shorten loan duration Cash-Out Refinance Access home equity as cash Debt consolidation or home improvements FHA Streamline Refinance Simplified FHA refinance Current FHA borrowers reducing payment VA IRRRL Rate reduction for VA loans Eligible military borrowers Conventional Refinance Flexible refinance structure Remove PMI or adjust loan structure

Understanding which structure fits your situation is often more important than simply looking for the lowest advertised rate.

Rate-and-Term Refinance A rate-and-term refinance replaces your current mortgage with a new loan that changes either the interest rate, the loan term, or both.

This refinance does not provide cash back to the borrower.

Common reasons homeowners choose this option include:

Potentially lowering the interest rate Reducing monthly payments Switching from a 30-year loan to a shorter term Moving from an FHA loan to a conventional loan For homeowners focused on long-term savings, rate-and-term refinancing is typically the most common strategy.

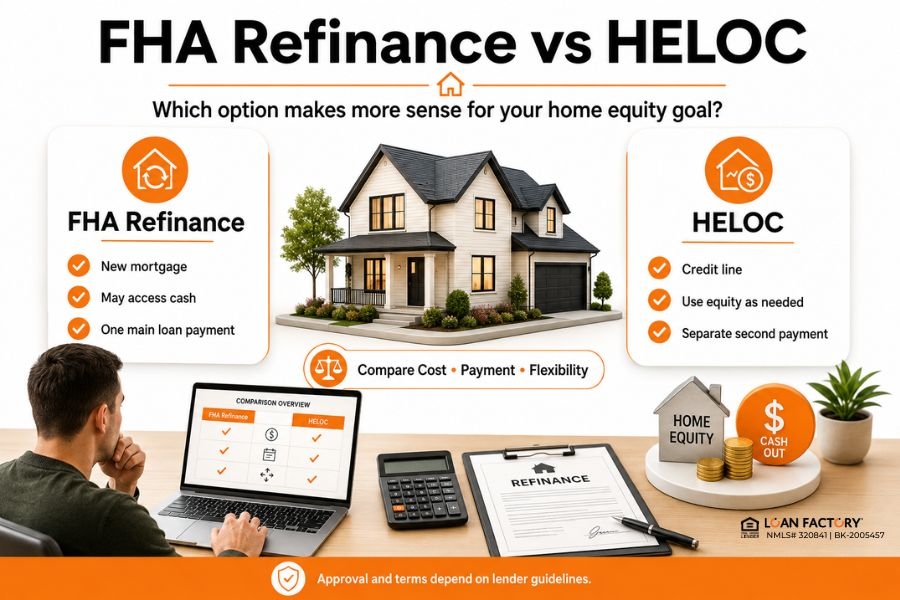

Cash-Out Refinance A cash-out refinance allows homeowners to borrow more than their remaining mortgage balance and receive the difference as cash.

The funds can be used for many purposes, such as:

Home renovations Debt consolidation Business investments Large planned expenses Approval for cash-out refinancing typically depends on several factors, including:

Available home equity Credit profile Property value Loan program guidelines Lenders generally require more equity for cash-out refinancing than for rate-and-term refinancing.

FHA Streamline Refinance The FHA Streamline Refinance program is designed for homeowners who currently have an FHA loan.

This program may allow simplified documentation requirements, depending on the borrower’s situation.

Homeowners often consider FHA streamline refinancing when:

Interest rates improve Monthly payments may decrease The borrower wants a simplified refinance process However, FHA mortgage insurance may still apply depending on loan structure. Many borrowers later refinance into a conventional loan once they build sufficient equity.

VA IRRRL Refinance The VA Interest Rate Reduction Refinance Loan (IRRRL) is available to eligible borrowers who currently have a VA loan.

This refinance option is commonly used to:

Reduce interest rates Adjust loan terms Simplify documentation requirements Eligibility depends on VA loan guidelines and lender requirements.

When Does Refinancing a Mortgage Make Sense? Refinancing tends to make the most sense when several financial factors align.

Based on many refinance scenarios reviewed by lending teams, homeowners often refinance when:

✔ They plan to stay in the home long enough to pass the break-even point

On the other hand, refinancing may be less beneficial when:

Closing costs exceed projected savings The homeowner plans to move soon The new loan significantly extends the repayment timeline A refinance should typically be evaluated as a long-term financial decision rather than a short-term rate change.

How Much Equity Do You Need to Refinance? Equity requirements vary depending on the refinance program and lender guidelines.

Refinance Goal

Typical Equity Considerations

Rate-and-term refinance Often allows higher loan-to-value ratios Cash-out refinance Typically requires more equity FHA to Conventional refinance Often evaluated near 20% equity if removing mortgage insurance

Actual eligibility depends on underwriting guidelines and lender overlays.

Homeowners often monitor their home value and loan balance to determine when refinancing may become beneficial.

Costs of Refinancing a Mortgage Refinancing usually includes several closing cost components.

Common refinance costs include:

Lender fees Title and escrow fees Recording costs Prepaid interest Property appraisal (in many cases) Some refinance structures allow certain costs to be:

Rolled into the new loan balance Offset through pricing adjustments Because refinance costs vary between lenders, homeowners should compare total loan cost and break-even timing, not just interest rate.

2026 Market Insight: What Lending Teams Are Seeing In recent refinance reviews across different U.S. markets, several trends have emerged.

Many homeowners are exploring refinancing primarily to:

Remove FHA mortgage insurance after gaining equity Consolidate higher-interest consumer debt through structured cash-out refinancing Improve loan flexibility after credit scores improve Adjust mortgage structure rather than simply chasing lower rates Another consistent observation is that small pricing differences between lenders can significantly affect the break-even timeline.

Even minor changes in pricing can shift the cost recovery period by months or years, which is why comparing lenders often plays a critical role in refinancing decisions.

How to Compare Refinance Mortgage Options When evaluating refinance options, homeowners often focus on several key factors.

Important comparison points include:

Interest rate and APR Total closing costs Break-even timeline Long-term interest paid Mortgage insurance impact Loan flexibility and lender overlays Rather than focusing only on advertised rates, experienced borrowers often compare total loan structure and long-term cost.

Why Comparing Multiple Lenders Matters for Refinancing Understanding how refinancing works is only the first step.

In practice, many homeowners discover that loan pricing, lender overlays, and refinance structures vary significantly across lenders. These differences can impact the overall cost of refinancing and how quickly savings offset closing costs.

Working with a platform that compares multiple lenders can make it easier to evaluate real refinance options instead of relying on a single bank’s pricing.

Why Homeowners Choose Loan Factory When Exploring Refinance Mortgages When reviewing refinance scenarios, comparing multiple lenders can help homeowners identify more competitive loan structures.

Loan Factory operates as a mortgage brokerage platform that compares options across 240+ wholesale lenders, helping borrowers evaluate refinance scenarios side-by-side.

Homeowners working with Loan Factory may benefit from:

Transparent side-by-side lender comparisons Zero application or junk fees Local loan advisors who help review refinance scenarios Real-time pricing powered by the MOSO mortgage platform Guidance from a lending platform led by Thuan Nguyen, recognized as the #1 Loan Officer in the U.S. Instead of guessing whether refinancing is worthwhile, homeowners can review real refinance numbers and evaluate their options clearly.

Take the Next Step If you're considering a refinance mortgage, the best next step is reviewing your individual scenario and comparing available loan options.

Apply online: https://www.LoanFactory.com/apply https://www.LoanFactory.com/quote www.loanfactory.com/mortgage-rate-alert

Based on real refinance scenarios reviewed by Loan Factory’s lending team helping homeowners evaluate rate-and-term and cash-out refinance options across multiple U.S. housing markets.

Disclaimer

This article is for informational purposes only and not a commitment to lend. Mortgage approval depends on credit, underwriting, property eligibility, and investor guidelines. Terms and conditions apply.

FAQ: Refinance Mortgage