Cash-Out Refinance : How It Works and When It Makes SenseA cash-out refinance replaces your current mortgage with a larger new first mortgage and converts part of your available home equity into cash. The new loan pays off your existing mortgage, eligible liens, and closing costs, and you receive the remaining proceeds after closing.

At Loan Factory, we help you compare cash-out mortgage programs based on your home equity, current mortgage rate, income, credit, monthly debts, property, and financial goals. A cash-out home refinance can provide useful funds, but replacing your current mortgage should make sense beyond the cash you receive.

Key Takeaways A cash-out refinance replaces your existing first mortgage with a larger new mortgage. The amount available depends on your property value, mortgage payoff, loan-to-value limit, liens, and closing costs. Lenders also review your credit, income, monthly debts, mortgage history, property, and ownership period. A home equity loan or HELOC may be worth comparing when you want to preserve your current first-mortgage rate. Important Note: Cash-out refinance eligibility, rates, fees, loan amounts, loan-to-value limits, ownership requirements, and available programs vary by lender, investor, property, occupancy, state, and borrower profile. This article is for educational purposes and is not a commitment to lend.

What Is a Cash-Out Refinance? A cash-out refinance is a mortgage transaction in which you replace your current home loan with a larger new first mortgage and receive part of the difference in cash. It allows you to access equity without selling the property, but it also increases or restructures the debt secured by your home.

Home equity is generally the difference between your property’s current value and the total amount of mortgage debt secured by it.

For example:

Estimated property value: $500,000 Current first mortgage balance: $275,000 New cash-out mortgage: $375,000 The new loan first pays off the existing $275,000 mortgage. Closing costs, prepaid expenses, taxes, subordinate liens, and other required charges are then deducted before the remaining proceeds are provided to you.

The Consumer Financial Protection Bureau describes cash-out refinancing as taking a larger mortgage, using part of it to pay off the current loan, and receiving the remaining amount in cash. The CFPB also notes that the transaction can extend the time needed to repay the mortgage and may increase the monthly payment.

Quick Answer: The cash-out refinance meaning is simple: you replace your existing mortgage and convert part of your home equity into cash through one larger first mortgage.

How Does a Cash-Out Refinance Work? A cash-out refinance works by using a new mortgage to pay off your current home loan and release part of your eligible equity. The lender determines the maximum new loan amount after reviewing your property value, existing liens, credit, income, monthly debts, mortgage history, and applicable loan-to-value limits.

The process usually follows these steps:

Estimate your current property value. Confirm the payoff balances of all existing liens. Review your credit, income, assets, and monthly debts. Determine which refinance programs fit your profile. Complete an appraisal or another approved property valuation. Submit the borrower and property documents for underwriting. Pay off the current mortgage at closing. Receive the remaining eligible proceeds after the applicable waiting period. A cash-out mortgage is different from a second mortgage. Your old first mortgage is paid off and replaced rather than left in place.

How Is the Cash Amount Calculated? The cash available is based on the maximum permitted new mortgage minus your current payoff, subordinate liens being paid, closing costs, prepaid expenses, taxes, and other charges included in the transaction.

A simplified formula is:

New mortgage amount − mortgage payoff − other liens − closing expenses = estimated cash proceeds

Suppose:

New mortgage: $400,000 Current first mortgage payoff: $285,000 HELOC payoff: $20,000 Estimated closing expenses: $12,000 The estimated cash proceeds would be:

$400,000 − $285,000 − $20,000 − $12,000 = $83,000

Illustrative Example: This simplified calculation is for educational purposes only. Actual property value, loan amount, rates, payments, fees, payoff figures, and cash proceeds depend on underwriting and current lender or investor guidelines.

What Is Home Equity? Home equity is the portion of your property’s value that is not covered by home-secured debt. It increases when you pay down your mortgage, the property appreciates, or both. A cash-out refinance converts part of that equity into new mortgage debt.

A simplified equity calculation is:

Estimated property value − total mortgage balances = gross home equity

For example:

Property value: $600,000 First mortgage: $330,000 HELOC: $30,000 Gross home equity:

$600,000 − $360,000 = $240,000

Gross equity is not the same as the amount you can receive.

The lender generally requires equity to remain after closing, and the permitted amount depends on:

Loan program Occupancy Property type Number of units Credit profile Loan amount Existing liens Appraised value Lender overlays How Much Equity Can You Cash Out? You generally cannot withdraw all the equity in your home. Cash-out refinance programs establish a maximum loan-to-value ratio, which limits the new mortgage to a percentage of the property’s appraised value.

Loan-to-value ratio is calculated as:

New first mortgage ÷ property value = LTV

For example:

Property value: $650,000 New mortgage: $487,500 The LTV is:

$487,500 ÷ $650,000 = 75%

Fannie Mae explains that maximum LTV depends on factors including credit score, mortgage product, occupancy, and the number of units in the property.

Primary residences can generally support more leverage than:

Second homes Investment properties Two- to four-unit properties Manufactured homes Properties with unique characteristics Transactions with higher credit or repayment risk At Loan Factory, we help you estimate the maximum loan amount and expected proceeds before you decide whether to move forward. The appraisal and final underwriting determine the actual amount available.

What Do Lenders Review? Lenders review your home equity, credit, income, monthly debts, mortgage payment history, property, occupancy, title history, and requested loan structure. The purpose is to confirm that the property supports the new mortgage and that the resulting payment fits the applicable underwriting requirements.

Factor

What the lender reviews

Why it matters

Property value Appraisal or approved valuation Determines available equity Mortgage balances First mortgage, HELOC, and other liens Establishes the amount that must be paid off Credit Scores, payment history, and major credit events Affects eligibility, pricing, and permitted leverage Income Employment, self-employment, retirement, rental, or other eligible income Supports the ability to repay Debt-to-income ratio Monthly debts compared with qualifying income Measures payment capacity Mortgage history Recent on-time or late housing payments Shows how current housing debt has been managed Assets and reserves Funds remaining after closing Can provide a financial cushion Ownership period How long the borrower has held title Some programs impose seasoning requirements Property type Occupancy, units, title, condition, and marketability Affects program eligibility and maximum LTV Loan purpose Intended use and requested amount Helps determine whether the structure fits the borrower’s needs

Cash-out refinance standards are generally stricter than rate-and-term refinance requirements because the borrower is increasing the loan balance and withdrawing equity.

What Credit Score Do You Need? There is no single minimum credit score for every cash-out refinance. Conventional, FHA, VA, portfolio, and non-QM programs use different standards, and lenders can add their own credit requirements based on the property, occupancy, loan amount, LTV, and complete borrower profile.

The lender may review:

Mortgage credit scores Recent late payments Revolving credit utilization Collections and charge-offs Bankruptcies Foreclosures Short sales Loan modifications Age and number of credit accounts Recent credit inquiries Disputed accounts Mortgage or rental payment history A stronger credit profile can provide:

More lender choices More favorable pricing Greater LTV flexibility Lower reserve requirements Access to larger loan amounts More options for second homes or investment properties A lower score does not necessarily prevent a refinance with cash out, but it can reduce the available loan amount or require more equity and reserves.

What Income Is Needed? You need enough stable, eligible income to support the new mortgage payment and your other monthly obligations. The lender verifies income using documents appropriate for your employment, self-employment, retirement, rental activity, or other qualifying income source.

W-2 Employees Documents can include:

Recent pay stubs W-2 forms Employment verification Bank statements Tax returns when required Self-Employed Homeowners Documents can include:

Personal tax returns Business tax returns K-1 forms Profit-and-loss statements Balance sheets Business bank statements Proof of business ownership Business registration or licensing Eligible borrowers can also explore alternative-documentation programs such as:

Bank statement refinance 1099 income refinance P&L-only refinance Asset-based qualification DSCR refinance for an investment property Alternative documentation does not mean no documentation. The lender still reviews the complete borrower, income method, property, credit profile, and proposed loan.

Retired Homeowners Documents can include:

Social Security documentation Pension statements Retirement account statements Annuity records Bank statements Tax returns when applicable The lender generally needs to determine that qualifying income is documented and likely to continue for the period required by the selected program.

How Does Debt-to-Income Ratio Affect a Cash-Out Mortgage? Debt-to-income ratio compares your required monthly debts with your gross qualifying monthly income. The proposed mortgage payment and your other obligations are combined to determine whether the new cash-out mortgage fits the applicable underwriting standards.

Monthly obligations can include:

New mortgage principal and interest Property taxes Homeowners insurance Mortgage insurance Homeowners association dues Credit-card minimum payments Auto loans Student loans Personal loans Other mortgages Alimony or child support when applicable Other recurring obligations required by the program A simplified formula is:

Total monthly debt payments ÷ gross qualifying monthly income = DTI

Under current Fannie Mae cash-out guidance, a Desktop Underwriter casefile with a DTI above 45% requires six months of reserves. This is a Fannie Mae-specific requirement rather than a universal rule for every cash-out program.

Reducing selected monthly debts can strengthen the application, but large payoffs should be reviewed with your Loan Officer before you use funds needed for closing or reserves.

→ Read more: how to calculate debt-to-income ratio for mortgage?

Does Mortgage Payment History Matter? Yes. Recent mortgage payment history can materially affect cash-out refinance eligibility because the lender is replacing your current housing debt with a larger mortgage obligation. Active delinquencies, recent late payments, incomplete repayment plans, or recent forbearance can limit available options.

The lender can review:

Whether the current mortgage is paid as agreed The number and severity of late payments How recently a delinquency occurred Whether the loan was in forbearance Whether the mortgage was modified Whether a repayment plan remains active Whether property taxes and insurance are current Continue making your current mortgage payments until the servicer confirms that the loan has been paid off. Starting a refinance application does not suspend your existing payment obligations.

How Long Must You Own the Home? Ownership and mortgage seasoning requirements depend on the program. Some conventional cash-out refinances require a borrower to have held title for at least six months, while the existing first mortgage being paid off may also need to be at least 12 months old.

Under Fannie Mae’s cash-out refinance guidance dated December 10, 2025:

An existing first mortgage being paid off generally must be at least 12 months old. At least one borrower generally must have held title for six months before the new loan is disbursed. Defined exceptions can apply for inheritance, certain legal awards, qualifying LLC or trust ownership, and delayed financing. Freddie Mac maintains its own requirements for ownership, title history, existing liens, and cash-out refinance transactions.

What Is Delayed Financing? Delayed financing is a specialized exception that can allow an eligible homeowner who recently purchased a property without mortgage financing to recover documented purchase funds through a cash-out refinance before the standard ownership period ends.

Under Fannie Mae rules, the original purchase and new refinance must meet requirements concerning:

Arm’s-length transaction Documented source of purchase funds Title ownership Existing liens Original purchase price New mortgage amount Use of borrowed or gifted purchase funds Delayed financing is not automatic. The lender must carefully review the original purchase and source-of-funds documents.

Is an Appraisal Required? A property valuation is generally needed because the lender must establish the home’s current value before calculating the maximum new mortgage and available cash. Depending on the lender and program, this can involve a full appraisal or another approved valuation method.

The valuation can consider:

Recent comparable sales Property condition Location Living area Lot size Improvements Number of units Marketability Health and safety concerns Permitted and unpermitted additions An online estimate is useful for early planning, but it does not determine the value used for final underwriting.

If the appraisal is lower than expected, you can receive:

Less cash A smaller permitted loan A higher LTV Different pricing A request to restructure the transaction A result that no longer meets the selected program What Can You Use the Cash For? Cash-out refinance proceeds can generally be used for many personal or financial purposes under conventional programs. The decision should be based on whether the benefit justifies replacing your current mortgage and increasing the debt secured by your property.

Common uses include:

Home improvements Debt consolidation Education expenses Medical costs Business investment Emergency expenses Purchasing another property Paying off a second mortgage Buying out a co-owner Building liquidity or reserves Fannie Mae allows eligible cash-out proceeds to be used for any purpose after required liens, closing costs, points, prepaid items, and other transaction amounts are addressed.

Can You Pay Off Credit Cards With Cash Out? Yes, homeowners can use cash-out proceeds to pay credit-card or other non-mortgage debt. However, doing so converts debt that may be unsecured into debt secured by the home and can stretch repayment across a much longer mortgage term.

The CFPB found that cash-out refinance borrowers frequently used proceeds to pay down credit cards and auto loans. The agency also noted that the financial benefit depends on whether the cost of extracting the equity is lower than the cost of continuing to repay the existing debts.

Before consolidating debt, compare:

Current debt interest rates New mortgage rate Origination and closing costs New repayment term Total interest over time Monthly cash-flow improvement Equity remaining after closing Risk of rebuilding credit-card balances Other repayment options A lower monthly payment does not necessarily mean a lower total cost.

What Types of Cash-Out Refinance Are Available? Homeowners can explore conventional, FHA, VA, portfolio, and non-QM cash-out refinance programs. The right structure depends on the existing mortgage, occupancy, property, credit, equity, income documentation, loan amount, and intended use of the funds.

Conventional Cash-Out Refinance A conventional cash-out refinance can replace an existing first mortgage, establish a mortgage on a property owned free and clear, pay eligible subordinate liens, finance closing costs, and provide additional equity proceeds.

Fannie Mae applies specific requirements related to:

Ownership period Existing mortgage age Property listing history Loan-to-value ratio Debt-to-income ratio Cash reserves Occupancy Property type Automated or manual underwriting Properties previously listed for sale must be removed from the market on or before the new loan’s disbursement date under current Fannie Mae rules.

Freddie Mac also treats cash-out refinancing as a distinct refinance type with its own borrower, title, lien, and transaction requirements.

→ Read more: FHA vs Conventional Refinance : Which Is Better?

FHA Cash-Out Refinance An FHA cash-out refinance allows an eligible homeowner to replace a current mortgage with a new FHA-insured mortgage and receive part of the available equity. It is intended for qualifying principal residences and requires FHA credit, income, property, appraisal, and mortgage-history review.

Current FHA policy limits standard cash-out refinance transactions to a maximum 80% LTV and CLTV, subject to FHA loan limits and other applicable requirements.

FHA cash-out financing can involve:

FHA appraisal Full income and credit underwriting Mortgage payment-history review Upfront mortgage insurance Annual mortgage insurance Principal-residence occupancy FHA property requirements Lender overlays An FHA cash-out refinance is different from an FHA streamline refinance . Streamline refinancing uses reduced credit documentation for an existing FHA-insured loan and does not provide substantial equity proceeds.

VA Cash-Out Refinance A VA-backed cash-out refinance allows an eligible Veteran, service member, or qualifying surviving spouse to replace an existing VA or non-VA mortgage with a new VA-backed loan and potentially access home equity.

The Department of Veterans Affairs states that the borrower must:

Qualify for a VA home loan Certificate of Eligibility Meet VA and lender credit and income requirements Occupy the property as a home Complete the lender’s appraisal and underwriting process The VA notes that the program can be used to refinance a non-VA loan into a VA-backed mortgage or obtain cash for needs such as debt, education, or home improvements.

A VA funding fee can apply unless the borrower qualifies for an exemption. Loan amounts, cash proceeds, rates, fees, seasoning, and net tangible benefit requirements depend on VA and lender guidelines.

Non-QM Cash-Out Refinance A non-QM cash-out refinance can provide alternatives for homeowners who do not fit conventional or government-backed documentation requirements. Private investors establish the income, credit, equity, reserve, property, and recent credit-event standards.

Available structures can include:

Bank statement refinance 1099 income refinance P&L-only refinance Asset depletion DSCR investment-property refinance Recent credit event programs ITIN mortgage programs Foreign national programs Depending on the program, you can encounter:

Lower maximum LTV More required equity Higher rates or fees Additional reserves Alternative income calculations Prepayment penalties where permitted Different property restrictions Non-QM does not mean no qualification or guaranteed approval.

→ Read more: Government home loan refinance programs

Cash-Out Refinance vs. Rate-and-Term Refinance A cash-out refinance provides equity proceeds beyond incidental closing adjustments. A rate-and-term refinance primarily changes the interest rate, loan term, or mortgage structure without allowing substantial cash to be withdrawn.

Feature

Cash-out refinance

Rate-and-term refinance

Main purpose Access home equity Change rate, term, or mortgage structure New balance Usually increases Generally tied closely to payoff and costs Cash received Substantial proceeds can be available Cash back is limited Equity requirement Generally higher Can allow more leverage Pricing Can be higher Can be more favorable Ownership rules Often stricter Can be more flexible Best fit Homeowner needs a lump sum Homeowner mainly wants new mortgage terms

Fannie Mae maintains separate eligibility rules for cash-out and limited cash-out refinance transactions.

Cash-Out Refinance vs. Home Equity Loan A cash-out refinance replaces your current first mortgage, while a home equity loan usually leaves that mortgage in place and adds a separate fixed-rate second mortgage. The better option depends heavily on your current first-mortgage rate and total borrowing cost.

Feature

Cash-out refinance

Home equity loan

Current first mortgage Replaced Remains in place Number of payments One new mortgage payment First mortgage plus second-loan payment New rate applies to Entire new mortgage balance Only the home equity loan Access to funds Lump sum Lump sum Loan position First mortgage Usually second lien Best fit Replacing the first mortgage also makes sense Preserving current first-mortgage terms is important

The CFPB notes that a home equity loan can be useful when a homeowner wants to access equity without replacing an existing lower-rate mortgage with a higher-rate cash-out refinance.

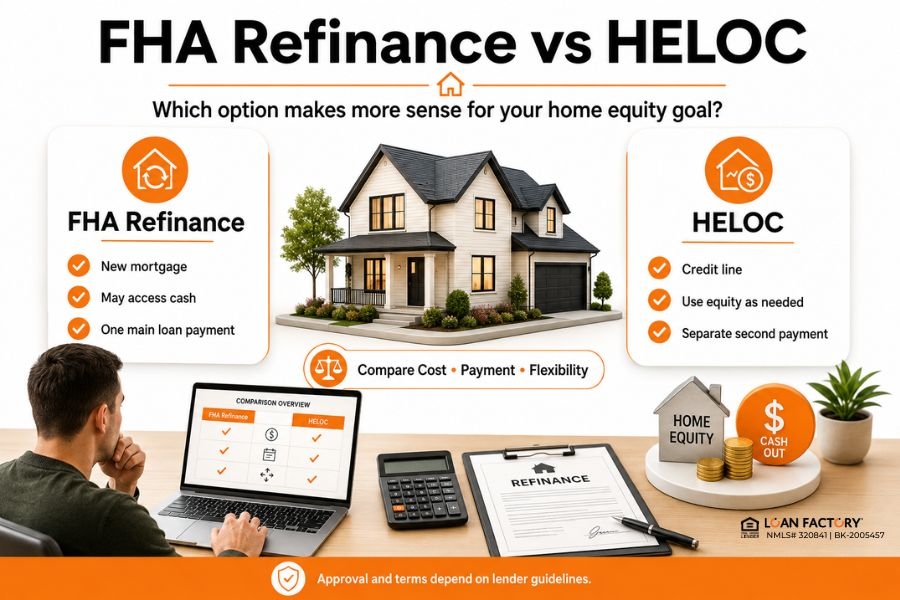

Cash-Out Refinance vs. HELOC A cash-out refinance provides one lump sum through a new first mortgage. A HELOC generally keeps the current mortgage in place and gives the homeowner a revolving credit line that can be borrowed, repaid, and reused during the draw period.

Feature

Cash-out refinance

HELOC

Current mortgage Replaced Usually remains Access to money Lump sum Revolving credit Interest rate Commonly fixed Commonly variable Interest applies to Full new mortgage Amount drawn Payment structure One new mortgage payment First mortgage plus HELOC payment Best fit Defined need for a lump sum Expenses occur over time

The CFPB describes a HELOC as a home-secured line that permits borrowing, repayment, and additional borrowing during the applicable period.

A HELOC’s variable rate can increase the payment. A cash-out refinance can offer a fixed-rate mortgage, but the new rate applies to the full first-mortgage balance.

Compare mortgage options before deciding which equity-access structure fits your current mortgage and financial goals.

Benefits of a Cash-Out Refinance The main benefit of a cash-out refinance is that it converts part of your home equity into a lump sum through one new first mortgage. It can also simplify multiple mortgage liens or other debts when the complete transaction supports your financial plan.

Potential benefits include:

Access to a large lump sum One first-mortgage payment Fixed-rate options Ability to pay off an existing HELOC or second mortgage Potential debt consolidation Funds for home improvements Options for primary, second, or investment properties Alternative-documentation programs for eligible borrowers Ability to refinance a property owned free and clear A potential benefit should be measured against the rate applied to your entire new mortgage balance, closing costs, loan term, and equity remaining after closing.

Risks and Drawbacks The main risks are replacing your current mortgage, increasing the amount secured by your home, paying closing costs, reducing available equity, and potentially extending the mortgage repayment period. The transaction can also increase total interest even when the monthly payment appears manageable.

Potential drawbacks include:

Higher mortgage balance Higher interest rate than the current mortgage Closing costs Longer repayment period Reduced home equity Larger total interest cost New appraisal and underwriting Risk of foreclosure if payments are not made Less flexibility during a future sale or refinance Possibility of rebuilding debts that were paid off The CFPB cautions that homeowners using equity to cover debt or living expenses can end up with less equity and continued financial strain if the underlying problem is not addressed.

How to Decide Whether to Refinance With Cash Out A cash-out refinance can make sense when you need a defined amount, can comfortably afford the new mortgage, will retain sufficient equity, and have compared the transaction with second-mortgage and non-borrowing alternatives.

Ask these questions:

How much money do I actually need? What is my current mortgage rate? What rate will apply to the full new balance? How much will the monthly payment change? What are the total closing costs? Will the mortgage term restart? How much total interest will I pay? How much equity will remain? How long do I expect to keep the home? Would a home equity loan preserve better first-mortgage terms? Would a HELOC provide more flexible access? Could waiting improve my credit or property equity? Does the use of funds create lasting value? Use the Loan Factory mortgage calculator to compare estimated loan amounts, terms, and principal-and-interest payments.

Calculator results are estimates and do not include every cost or determine loan eligibility.

How to Apply for a Cash-Out Refinance Start by estimating your equity, clarifying how much cash you need, and completing a full mortgage review. Your Loan Officer can then compare programs, estimate the proceeds, and identify the borrower and property documents required for underwriting.

Step 1: Clarify Your Goal Determine:

How much cash you need How the funds will be used Whether the need is one-time or ongoing How much equity you want to preserve Whether replacing the current mortgage makes sense Step 2: Review Your Current Mortgage Gather:

Current mortgage statement Interest rate Remaining term Approximate payoff HELOC or second-mortgage statements Information about prepayment terms Mortgage payment history Step 3: Estimate Your Property Value Use recent sales and online estimates as a preliminary guide.

The lender’s approved appraisal or valuation determines the value used for underwriting.

Step 4: Review Credit and Monthly Debts Check for:

Credit-report errors Recent late payments High revolving balances Newly opened accounts Mortgage delinquencies Major derogatory credit events Avoid opening new debt before and during the mortgage process.

Step 5: Prepare Income and Asset Documents Depending on your profile, documents can include:

Pay stubs W-2 forms Tax returns Business returns Bank statements Retirement accounts Profit-and-loss statements Business bank statements Social Security or pension documentation Step 6: Compare Programs Review:

Conventional cash-out refinance FHA cash-out refinance VA cash-out refinance Non-QM cash-out refinance Home equity loan HELOC Keeping the existing mortgage unchanged Step 7: Complete the Property Valuation The appraisal or approved valuation confirms whether the property supports the new loan amount.

Step 8: Review the Loan Estimate Compare:

Interest rate APR Monthly payment Loan amount Closing costs Cash to close Estimated cash proceeds Loan term Prepayment terms Mortgage insurance or funding fee Step 9: Complete Underwriting The lender verifies the borrower, property, title, liens, insurance, income, assets, credit, and transaction.

Step 10: Close and Receive the Funds For many refinances secured by a principal residence, federal law provides a three-business-day rescission period after signing before the lender disburses the proceeds. Saturdays generally count as business days, but Sundays and federal legal holidays do not. Specific transaction types and properties can be treated differently.

Common Cash-Out Refinance Mistakes The most common mistakes include focusing only on the cash received, failing to compare the new rate with the existing mortgage, withdrawing more equity than needed, overlooking closing costs, and extending short-term debt over a long mortgage term.

Comparing Only the Monthly Payment A lower payment can be created by extending the repayment term.

Compare the total interest and projected payoff date.

Ignoring the Existing Mortgage Rate A higher new rate applies to the entire mortgage balance, not only the additional cash.

Compare a home equity loan or HELOC when preserving the current first mortgage matters.

Borrowing the Maximum Amount Maximum approval does not mean the maximum loan supports your long-term goals.

Preserving equity can provide flexibility for future needs.

Paying Off Debt Without Changing Spending Debt consolidation can fail when credit-card balances return after closing.

You can end up with a larger mortgage and new revolving debt.

Assuming the Online Value Is Final The lender’s approved valuation determines the transaction.

A lower appraisal can reduce the loan amount and cash proceeds.

Overlooking the New Loan Term Restarting a 30-year mortgage can increase total interest, even when the new monthly payment seems affordable.

How Loan Factory Helps With a Cash-Out Refinance At Loan Factory, we help you evaluate more than the amount of cash you can receive. Our Loan Officers review your current mortgage, available equity, property value, credit, income, monthly debts, cash needs, and long-term goals before comparing available programs.

We help you:

Estimate your available home equity Compare conventional, FHA, VA, and non-QM options Understand LTV, CLTV, title, and ownership requirements Review income and debt-to-income calculations Estimate proceeds after liens and closing costs Compare your current and proposed mortgage payments Evaluate cash-out refinancing against a HELOC or home equity loan Identify documents needed for underwriting Explore alternative income documentation when appropriate Build a preparation plan when refinancing immediately is not the right path Use TERA to support pricing, document collection, communication, and loan progress We explain the immediate benefit and the long-term cost, so you can decide whether replacing your current first mortgage supports your goals.

Your rate, loan amount, payment, and proceeds will depend on your application, property, appraisal, underwriting results, and selected lender’s guidelines.

Compare mortgage options or call or text (660) 333-3333 to discuss your home equity and refinance goals with a Loan Factory mortgage professional.

A cash-out refinance can be a practical choice when the funds serve a clear purpose, the new payment fits your budget, enough equity remains, and replacing your current mortgage creates a reasonable overall financial structure.

It can fit homeowners who:

Need a defined lump sum Want to consolidate existing mortgage liens Can afford the new payment Expect to keep the property long enough to justify the costs Have compared the transaction with second-mortgage options Understand the effect on their loan term and total interest Another option may be more appropriate when:

Your current mortgage rate is substantially more favorable You need access to funds gradually Closing costs outweigh the expected benefit The new payment would strain your budget You expect to sell the property soon You need only a relatively small amount Waiting could improve your credit or equity position Conclusion A cash-out refinance allows you to replace your current mortgage with a larger new first mortgage and receive part of your eligible home equity as cash. The amount available depends on your property value, current payoff, liens, closing costs, permitted LTV, and complete financial profile.

The cash can support home improvements, debt consolidation, education, business needs, or other goals, but it also increases or restructures debt secured by your home.

At Loan Factory, we help you compare a cash-out home refinance with conventional, FHA, VA, non-QM, HELOC, and home equity loan options. We explain the payment, costs, equity impact, and long-term tradeoffs before you choose a path.

Apply online or call or text (660) 333-3333 to begin your cash-out mortgage review.

Experience Note When our Loan Officers review a refinance with cash out, we do not focus only on the property value or the amount requested.

We also review the current mortgage rate, payoff balance, available equity, income, monthly debts, credit, payment history, closing costs, equity remaining after closing, expected time in the home, and second-mortgage alternatives.

This complete comparison helps you understand both the immediate proceeds and the long-term impact of replacing your mortgage.

Sources Consumer Financial Protection Bureau guidance and research on cash-out refinancing, home equity, debt consolidation, HELOCs, and home equity loans. Fannie Mae Selling Guide requirements for cash-out and limited cash-out refinance transactions, ownership, seasoning, reserves, and property eligibility. Freddie Mac Seller/Servicer Guide requirements for cash-out refinance mortgages. U.S. Department of Housing and Urban Development guidance on FHA cash-out and streamline refinance mortgages. U.S. Department of Veterans Affairs guidance on VA-backed cash-out refinance loans. Disclaimer: This content is for educational and informational purposes only and is not financial, tax, legal, credit, or housing counseling advice, a commitment to lend, or a guarantee of approval. Mortgage programs, rates, fees, payments, loan-to-value limits, income calculations, ownership requirements, cash proceeds, documentation, and eligibility are subject to change and vary based on credit, income, assets, debts, property, occupancy, loan purpose, appraisal, underwriting, lender overlays, and investor guidelines.

About the Author Loan Factory Mortgage Education Team

Loan Factory is a technology-powered mortgage platform helping borrowers compare mortgage options through a broad wholesale lender network.

The Loan Factory Mortgage Education Team helps homeowners understand cash-out refinancing, home equity, loan-to-value ratios, mortgage qualification, closing costs, and the tradeoffs between first-mortgage refinancing and second-mortgage options.

Frequently Asked Questions