Refinancing can be a smart financial move—but only when it aligns with your long-term goals. In 2025, with rate movements shifting frequently and new lender guidelines in place, many homeowners wonder whether refinancing is still worth it.

This guide breaks down the pros and cons of refinancing your mortgage , how the process works, and when it may or may not make sense.

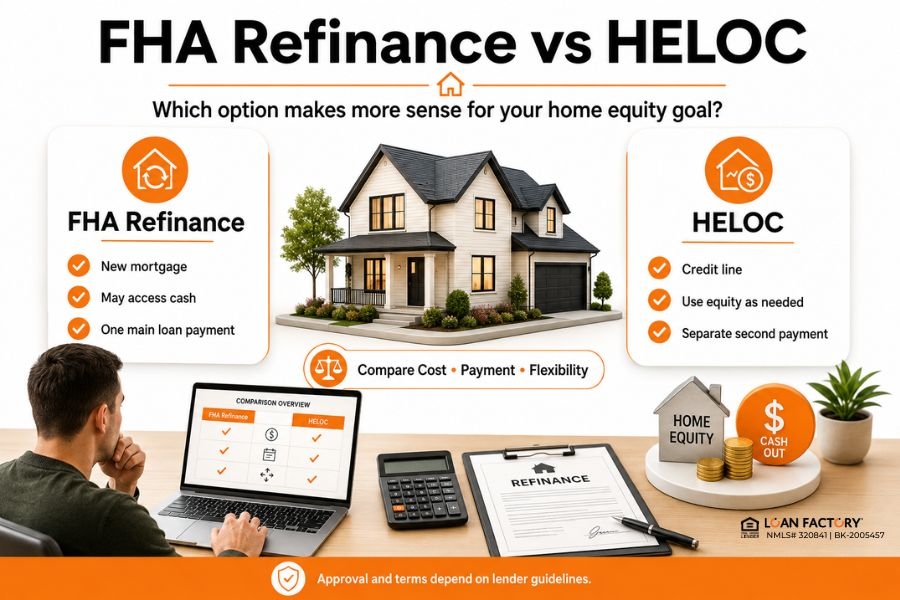

What Is a Mortgage Refinance? A refinance replaces your current mortgage with a new one—usually to change your rate, loan term, or loan type, or to tap home equity.

Refinancing is optional, and approval depends on credit, income, equity, and lender guidelines.

(Informational purposes only. Not a commitment to lend.)

Pros of Refinancing Your Mortgage 1. Potentially Lower Monthly Payments If market rates are lower than your current rate, you may qualify for a reduced payment. Lower payments can improve cash flow and long-term affordability.

2. Reduce Your Interest Cost Over Time Refinancing into a shorter term (15- or 20-year) may reduce the total interest you pay, even if the payment is higher.

3. Switch From an Adjustable Rate to a Fixed Rate If you currently have an ARM, refinancing into a fixed mortgage can offer more stability—especially in a rising-rate environment.

4. Tap Into Home Equity (Cash-Out Refinance) You can access your home equity for:

Home improvements Debt consolidation Major expenses This may offer better terms compared to personal loans or credit cards.

5. Remove Private Mortgage Insurance (PMI) If your home value has increased, refinancing may eliminate PMI and reduce your payment.

→ Read more: How Can I Reduce My Mortgage Payment?

Cons of Refinancing Your Mortgage 1. Closing Costs Refinances typically include lender fees, title fees, and third-party costs. These can often be rolled into the loan, but doing so increases your balance.

2. Resetting Your Loan Term Starting a new 30-year term may increase your total interest paid, even with a lower monthly payment.

3. Qualification Requirements Approval depends on:

Current credit score Debt-to-income ratio Property value Not all borrowers will qualify under today’s guidelines.

4. Risk of Higher Rate if Market Shifts If you wait too long and rates rise, refinancing may no longer be beneficial.

5. May Not Make Sense If You Plan to Sell Soon If you’re moving within 1–3 years, the savings may not outweigh the upfront costs.

→ Read more: What Is the Waiting Period for a Rate-and-Term Refinance?

When Does Refinancing Make Sense? Homeowners often consider refinancing when:

Market rates drop below their current rate They want to switch from ARM to fixed They’ve built equity and want to remove PMI They want cash out for renovations or debt payoff They want to shorten their amortization schedule Always compare total cost vs. long-term savings.

→ Read more: Refinance Mortgage Broker Near Me

Why Choose Loan Factory for Your Refinance? Homeowners choose Loan Factory because our model is built to deliver transparent pricing, fast technology, and nationwide lender access—designed to save you time and help you compare smarter.

No application or junk fees – More of your money stays in your pocket. Compare 240+ lenders side by side – See options clearly in one place. Local loan advisors – Real people to walk you through stressful decisions. MOSO AI technology – Real-time pricing and faster, more transparent approvals. Backed by expertise – Loan Factory is led by Thuan Nguyen, the #1 loan officer in the U.S . We can help you explore refinance options, term changes, or new purchase strategies so you can move forward with a plan instead of stress.

Ready to Explore Your Refinance Options? Apply online: www.LoanFactory.com/apply

Check mortgage rates: www.LoanFactory.com/quote

Set up a rate alert: www.loanfactory.com/mortgage-rate-alert

For faster support, you can call or text us at (660) 333-3333

This content is for informational purposes only and not a commitment to lend. Loan terms, rates, and approval depend on credit, underwriting, and investor guidelines.

→ Read more: Home Loan Refinance: Is Now the Right Time for You to Check Your Rate?

FAQ