For many U.S. homeowners—especially first-time buyers—the monthly mortgage payment is the biggest line item in the household budget. So it’s no surprise the question comes up often:

“ How can I reduce my mortgage payment? ”

The good news: you may have more options than you think. Below are 10 Smart Strategies, that can legitimately help you reduce your monthly payment—while staying compliant and aligned with long-term financial goals.

1. Refinance When It Benefits You Refinancing remains one of the most effective ways to reduce your monthly payment—but only when the numbers make sense.

You may consider refinancing if:

Today’s available rates are meaningfully lower than your current rate You want to switch from a 15-year to a 30-year term Your credit score has improved Your property value has risen enough to remove mortgage insurance Always request a break-even analysis to understand how long it takes for monthly savings to offset any closing costs.

Note: This information is for educational purposes only and not a commitment to lend. Eligibility depends on credit, underwriting, and investor guidelines.

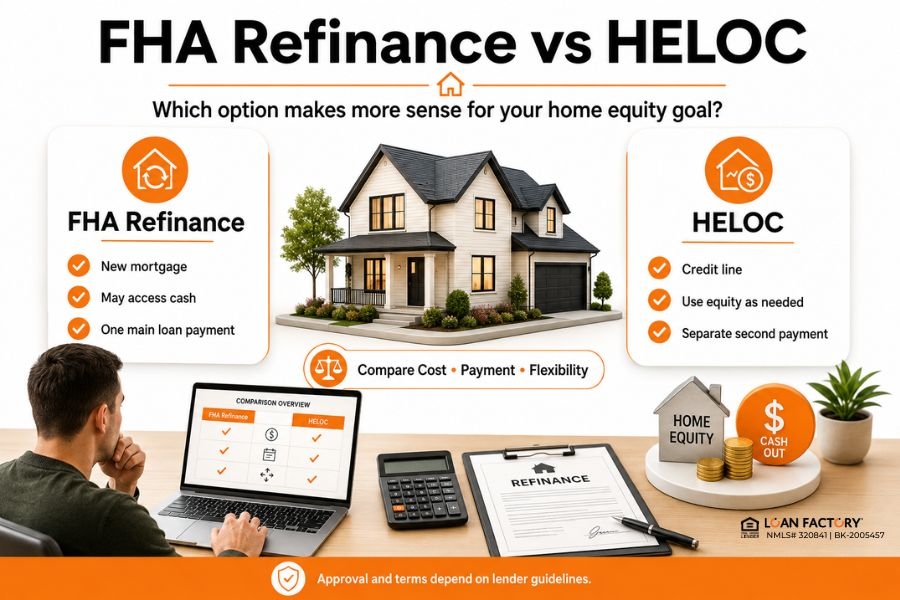

→ Read more: Does Refinancing Lower Your Monthly Payment?

Refinance When It Benefits You 2. Reduce or Remove PMI (Private Mortgage Insurance) PMI adds extra monthly cost for most buyers who put less than 20% down.

Ways to reduce or remove PMI:

Request PMI cancellation once you reach 20% equity Refinance into a new loan if your home value has increased Use an 80/10/10 structure to avoid PMI from the start Since PMI protects the lender—not the homeowner—removing it can be one of the fastest ways to lower your payment.

3. Compare Offers From Multiple Lenders Many borrowers overpay simply because they only check with one lender.

Borrowers who shop around often:

Save on upfront closing costs Receive more competitive pricing Increase long-term savings Mortgage brokers like Loan Factory compare 240+ wholesale lenders, giving you transparency and breadth that a single bank can’t match.

Compare Offers From Multiple Lenders 4. Lower Your Escrow Costs (Taxes & Insurance) Your mortgage payment includes:

Property taxes Homeowners insurance HOA dues (if applicable) If these costs go up, your monthly payment goes up—even if your interest rate stays the same.

Ways to reduce escrow:

Appeal your property tax assessment Shop around for more competitive insurance premiums Request an escrow review if your costs have recently decreased Each county and insurer has different rules, but annual reviews can help you stay on track.

5. Extend Your Loan Term for Lower Monthly Payments Extending your mortgage term (e.g., 15 → 30 years) spreads payments over a longer period, lowering your monthly cost.

This may be helpful if you need:

Immediate cash-flow flexibility Budget restructuring Temporary relief during higher interest-rate cycles However, extending the term increases the total interest paid over time—so consider how it fits into your long-term goals.

→ Read more: What Is the Waiting Period for a Rate-and-Term Refinance?

6. Use Free Rate Alerts to Time the Market Mortgage rates can fluctuate multiple times per day.

Set a target rate Receive instant notifications Lock when conditions match your goal Avoid watching the market constantly There’s no credit pull or cost to use the alert system—just smarter timing.

Set up a rate alert 7. Work With a Transparent, Data-Driven Mortgage Partner Reducing your mortgage payment is easier when you have access to the right tools and expertise.

Loan Factory provides:

Access to 240+ wholesale lenders Real-time pricing comparison Rate alerts Local loan advisors trained under Thuan Nguyen, #1 Loan Officer in the U.S. Technology designed around clarity and savings “A great mortgage isn’t just about the rate—it’s about how informed and supported you feel along the way.”

8. Improve Your Credit Score to Unlock Better Terms A stronger credit score can help you qualify for more favorable pricing when buying or refinancing.

Ways to strengthen credit:

Lower credit utilization Avoid new inquiries before applying Pay down revolving balances Keep older credit lines open Even modest improvements may impact eligibility, pricing adjustments, and mortgage insurance requirements.

9. Explore Different Loan Programs That May Reduce Your Monthly Cost Some homeowners can reduce their mortgage payment simply by choosing a different loan program, depending on eligibility:

FHA loan → Conventional refinance to remove MIPVA loan (for eligible veterans/military, no PMI)USDA loan (for eligible rural buyers, income and area limits apply)Conventional loan with better MI optionsSwitching investors for more flexible terms Each loan type has its own requirements, but exploring your options may uncover opportunities for lower monthly costs.

→ Read more: Government Home Loan Refinance Programs

10. Consider an ARM Loan (If It Fits Your Timeline) Adjustable-Rate Mortgages (ARMs) may offer lower introductory rates compared to fixed-rate loans.

This may be suitable if:

You plan to move before the first adjustment You expect to refinance later You want lower initial payments for short-term planning Always review adjustment caps, timelines, and risks with your loan advisor before choosing an ARM.

Why Choose Loan Factory? Loan Factory helps you save with a transparent, data-driven approach:

Zero application or junk fees Compare 240+ lenders instantly Local loan advisors for personalized guidance AI-powered MOSO platform for faster approvals & real-time pricing Trusted guidance from Thuan Nguyen , #1 Loan Officer in the U.S. Loan Factory makes the mortgage process clearer, faster, and more affordable for homebuyers nationwide.

Take the First Step Toward a Lower Monthly Payment If you’re asking, “How can I reduce my mortgage payment?”, now’s the perfect time to explore your options.

We’ll help you compare, understand, and choose the option that fits your financial goals.

Apply online: www.LoanFactory.com/apply

Check mortgage rates: www.LoanFactory.com/quote

Set up a rate alert: www.loanfactory.com/mortgage-rate-alert

For faster support, you can call or text us at (660) 333-3333

This content is for informational purposes only and not a commitment to lend. Loan terms, rates, and approval depend on credit, underwriting, and investor guidelines.

Loan Factory reviews Frequently Asked Questions (FAQ)