If you’re thinking about refinancing, you’re probably wondering:

“What actually happens when you refinance your home?”

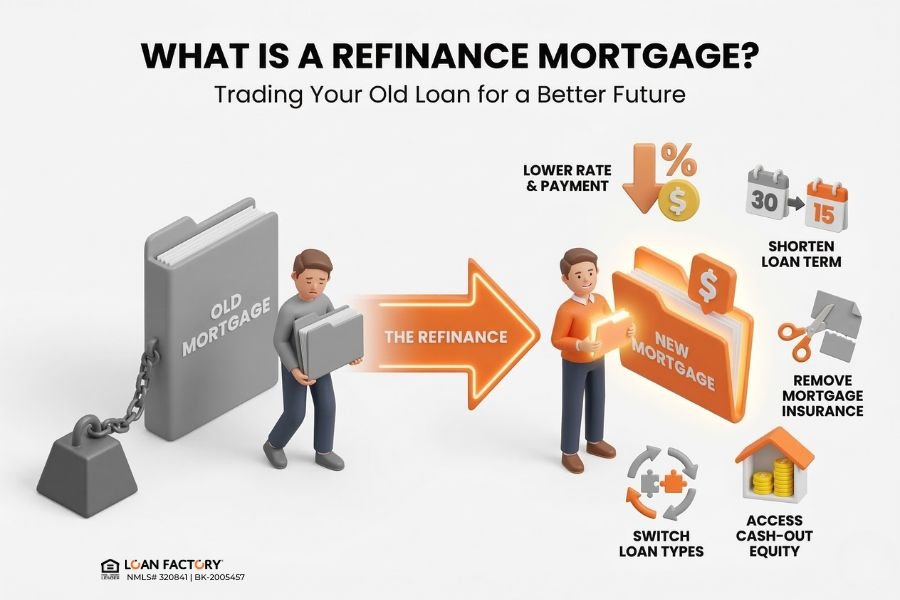

Refinancing isn’t just a simple switch—it’s a structured process where your current mortgage is replaced with a new one.

Understanding what happens behind the scenes can help you:

Avoid surprises Make better decisions Know what to expect at each step In this guide, we’ll walk through exactly what happens before, during, and after a refinance.

What Does It Mean to Refinance Your Home? When you refinance your home:

Your existing mortgage is paid off

You then begin making payments on the new loan instead of the old one.

This process changes:

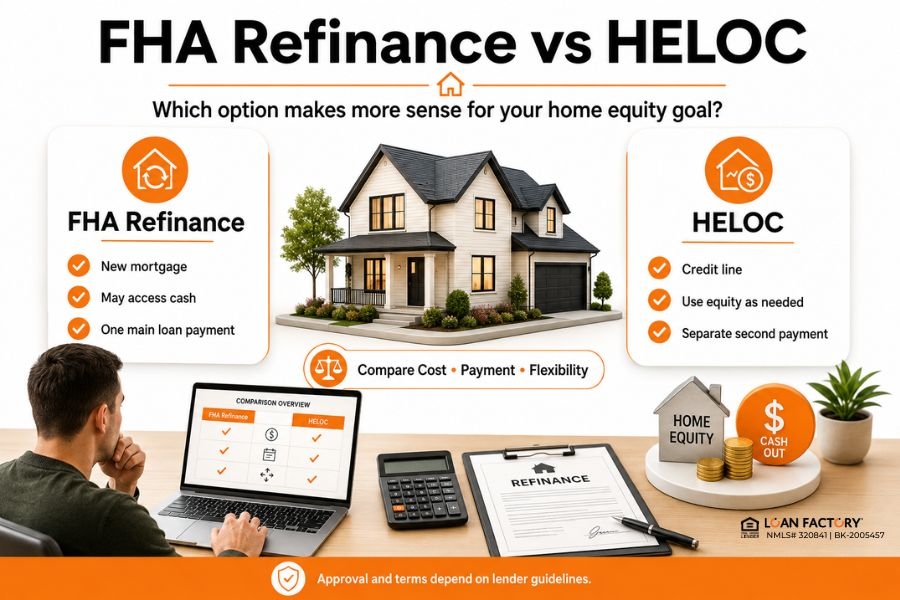

Your interest rate Your monthly payment Your loan term Your total loan cost → Read more: Best Refinance Home Loans in the U.S.

Step-by-Step: What Happens During a Home Refinance Here’s how the refinance process typically works:

Step 1: You Apply for a New Loan You start by submitting your information, including:

Income Credit profile Property details Current mortgage information At this stage, lenders evaluate what refinance options may be available.

Step 2: Your Loan Scenario Is Reviewed The lender (or broker) reviews:

Credit score Debt-to-income ratio Home value Loan-to-value ratio This determines which refinance programs you may qualify for.

Step 3: Home Value Is Verified In many cases, your home value is evaluated through:

An appraisal Automated valuation (depending on program) Your home value affects:

Equity Loan eligibility Pricing Step 4: You Lock Your Loan Terms Once you choose a refinance option, your loan terms may be locked.

This includes:

Interest rate Loan structure Pricing This step helps protect your loan terms from market changes.

Step 5: Underwriting and Approval The lender reviews your full file to confirm:

Income and employment Assets Property details Loan eligibility Additional documents may be requested during this stage.

Step 6: Closing Your Refinance Loan At closing:

You sign final loan documents Closing costs are finalized The new loan is officially created Your old mortgage is paid off using the new loan funds.

Step 7: After Closing (Important Step Many Miss) After closing:

Your old loan is fully paid off Your new loan becomes active You begin making payments under new terms In some cases:

There may be a short period before your first payment is due Escrow accounts may be restructured What Changes After You Refinance? After refinancing, several things may change:

Area

What May Change

Monthly payment May increase or decrease Interest rate May be lower or restructured Loan term May reset or shorten Mortgage insurance May be removed Cash flow May improve depending on structure

The outcome depends on how the new loan is structured.

Costs and Financial Impact of Refinancing Refinancing typically includes:

Lender fees Title and escrow costs Prepaid interest Appraisal (in many cases) Some costs may be:

Paid upfront Rolled into the loan Offset through pricing This is why evaluating total cost—not just monthly payment—is important.

What Happens to Your Old Mortgage? A common question:

Does your old loan just disappear?

Here’s what actually happens:

Your new lender pays off your existing mortgage The old loan is closed You no longer owe payments on the previous loan You now have a completely new mortgage agreement.

→ Read more: Does refinancing lower your monthly payment

Real-World Insight: What Homeowners Often Don’t Expect From real refinance scenarios:

The process is similar to getting a mortgage—but often faster Documentation requirements still apply Loan terms can vary significantly between lenders Final numbers may differ slightly from initial estimates Understanding the process helps reduce confusion and delays.

Why Understanding the Process Helps You Make Better Decisions When homeowners understand what happens during refinancing:

They ask better questions They compare options more effectively They avoid costly mistakes Knowledge leads to better refinance outcomes.

Why Comparing Lenders Matters in the Refinance Process Even though the process is similar across lenders:

Pricing differs Loan structures vary Approval flexibility changes The lender you choose can significantly impact your results.

Why Homeowners Choose Loan Factory for Refinancing If you're considering refinancing your home, comparing multiple lenders can give you a clearer picture of your options.

Loan Factory helps homeowners evaluate refinance scenarios across 240+ wholesale lenders, making it easier to see real loan structures.

Here’s how that helps:

Transparent side-by-side comparisons Zero application or junk fees Local loan advisors for personalized guidance Real-time pricing powered by MOSO Guidance from a platform led by Thuan Nguyen (#1 Loan Officer in the U.S.) Instead of guessing how refinancing works, you can review actual options based on your situation.

Take the Next Step If you're thinking about refinancing your home, the next step is reviewing your options.

Apply online: https://www.LoanFactory.com/apply https://www.LoanFactory.com/quote www.loanfactory.com/mortgage-rate-alert

Based on real refinance scenarios reviewed by Loan Factory’s lending team helping homeowners understand the refinance process, loan structure changes, and post-closing outcomes across multiple U.S. markets.

Disclaimer

This article is for informational purposes only and not a commitment to lend. Mortgage approval depends on credit, underwriting, property eligibility, and investor guidelines. Terms and conditions apply.

FAQ: What Happens When You Refinance Your Home