Refinancing a mortgage can be a powerful financial move—but timing is everything.

Many homeowners ask the same question:

When should you refinance your mortgage to actually save money or improve your loan structure?

The answer depends on more than just interest rates. Factors like equity, break-even timing, credit profile, and long-term plans all play a role.

In this guide, we’ll break down when refinancing makes sense, when it doesn’t, and how experienced lending teams evaluate real refinance scenarios.

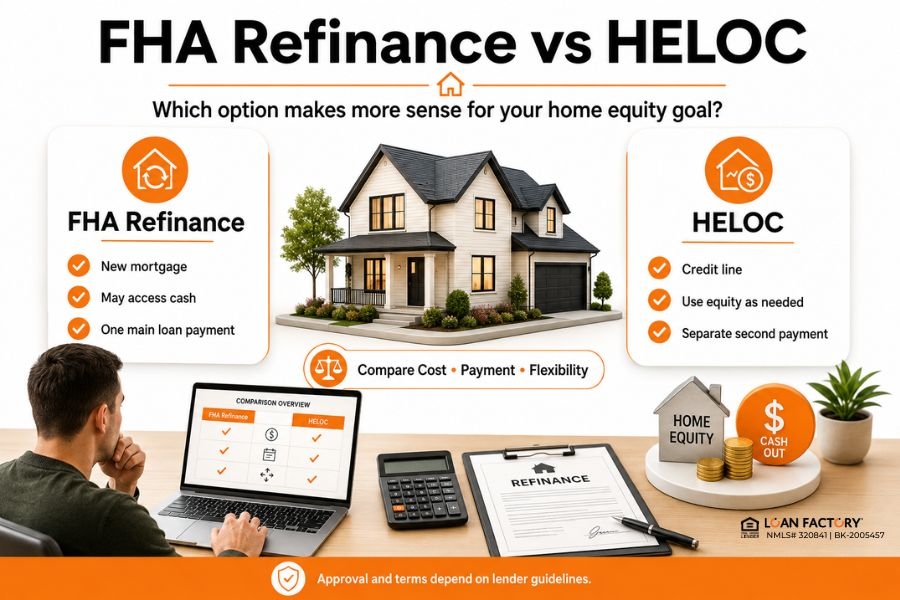

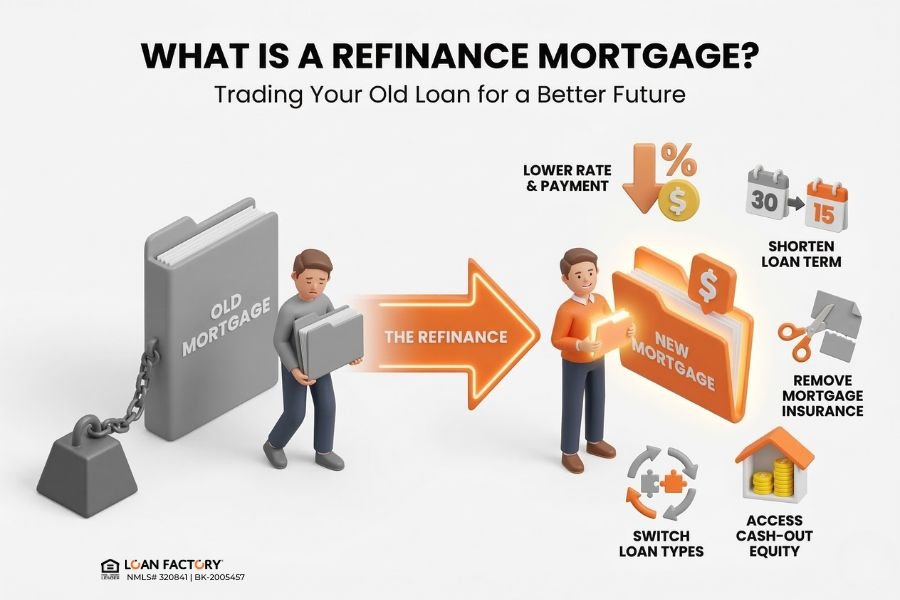

What Does It Mean to Refinance Your Mortgage? Refinancing means replacing your current mortgage with a new loan.

The new loan pays off your existing balance, and you begin making payments under new terms.

Homeowners typically refinance to:

Potentially lower their interest rate Reduce monthly payments Change loan terms (e.g., 30-year → 15-year) Remove mortgage insurance (PMI or FHA MIP) Access home equity through cash-out refinancing But refinancing only makes sense if it improves your overall financial position—not just your monthly payment.

→ Read more: Types of Refinance Loans

When Should You Refinance Your Mortgage? There’s no single “perfect time,” but based on real-world lending scenarios, refinancing often makes sense under these conditions:

1. When You Can Reach the Break-Even Point One of the most important factors is the break-even timeline.

This is the point where your monthly savings exceed the cost of refinancing.

Example: Closing costs: $6,000 Monthly savings: $200 Break-even: 30 months If you plan to stay in the home longer than 30 months, refinancing may make financial sense.

If you plan to move sooner, refinancing may not be beneficial.

2. When Interest Rates Improve (or Your Rate Is High) Even in a rising rate environment, refinancing can still make sense if:

Your current rate is significantly higher than today’s market range You previously bought during a higher-rate period You need to restructure your loan (not just lower rate) Important: A lower rate alone doesn’t guarantee savings—total cost matters.

3. When You Have Built Enough Equity Equity plays a major role in refinance eligibility and cost.

Scenario

Why It Matters

20%+ equity May allow removal of PMI or FHA MIP Higher equity Better loan options and pricing Low equity Limited refinance flexibility

Many homeowners refinance specifically to remove FHA mortgage insurance once they reach sufficient equity.

4. When Your Credit Score Has Improved If your credit profile has improved since you got your original mortgage, refinancing may help you:

Qualify for better loan pricing Access more loan options Improve overall loan structure Even moderate credit improvements can impact lender pricing.

5. When You Want to Remove Mortgage Insurance This is one of the most common refinance triggers.

For example:

FHA loans include mortgage insurance (MIP) Conventional loans may allow PMI removal at ~20% equity Many homeowners refinance from FHA to Conventional to eliminate monthly insurance costs.

6. When You Need to Access Home Equity A cash-out refinance may make sense when you need structured access to equity for:

Debt consolidation Home improvements Major financial planning However, this should be evaluated carefully, as it changes your loan balance and long-term cost.

7. When You Want to Change Loan Terms Refinancing can also help you adjust your financial strategy:

Switch from a 30-year loan to a shorter term Pay off your mortgage faster Stabilize payments (e.g., ARM → fixed rate) This is often used by homeowners focused on long-term wealth building rather than short-term savings.

When Refinancing May NOT Make Sense Refinancing isn’t always the right move.

It may not be beneficial if:

You plan to sell your home soon Closing costs outweigh potential savings Your new loan extends your payoff timeline significantly Your financial situation has not improved A refinance should always be evaluated based on total cost and long-term impact—not just monthly payment.

Real-World Insight: What Lending Teams Are Seeing Across many refinance scenarios reviewed recently, several patterns stand out:

Many homeowners refinance to remove FHA mortgage insurance after equity increases Cash-out refinancing is often used to consolidate high-interest debt Break-even timing has become more important in higher-rate environments Pricing differences between lenders can significantly impact long-term cost In practice, two lenders can offer similar rates—but very different total loan structures.

How to Decide If You Should Refinance Before refinancing, homeowners should evaluate:

How long they plan to stay in the home Total closing costs vs projected savings Equity position Credit profile Loan structure (not just rate) The goal is not just to refinance—it’s to make a better financial decision over time.

→ Read more: No-Closing-Cost Refinance | Lower Your Rate Without Upfront Costs

Why Comparing Lenders Is Critical Before Refinancing Understanding when to refinance is only part of the decision.

The next step is comparing real loan options across lenders, because:

Pricing varies significantly Lender overlays affect qualification Loan structures can change long-term costs Without comparison, homeowners may miss better options.

Why Homeowners Choose Loan Factory for Refinance Decisions If you're deciding whether to refinance, having access to multiple lender options can make a major difference.

Loan Factory operates as a mortgage brokerage platform that compares 240+ wholesale lenders, helping homeowners evaluate refinance scenarios clearly.

Here’s how that helps:

Transparent side-by-side lender comparisons Zero application or junk fees Local loan advisors to review your specific situation AI-powered MOSO platform for real-time pricing Guidance from a lending platform led by Thuan Nguyen (#1 Loan Officer in the U.S.) Instead of guessing whether refinancing makes sense, you can review actual numbers and make a confident decision.

Take the Next Step If you're wondering whether now is the right time to refinance, the best step is to review your specific scenario.

Apply online: https://www.LoanFactory.com/apply https://www.LoanFactory.com/quote www.loanfactory.com/mortgage-rate-alert

Based on real refinance scenarios reviewed by Loan Factory’s lending team helping homeowners evaluate rate-and-term and cash-out refinance options across multiple U.S. markets.

Disclaimer

This is for informational purposes only and not a commitment to lend. Terms depend on credit, underwriting, and investor guidelines.

FAQ: When Should You Refinance Your Mortgage?