When refinancing a mortgage, many homeowners face the same decision:

Should you refinance into another FHA loan — or switch to a conventional loan?

The right answer depends on:

Your equity Your credit score Your long-term plans Whether removing mortgage insurance is a priority In real refinance scenarios reviewed by our lending team, the “better” option often wasn’t about rate alone — it was about long-term structure.

Let’s compare both paths clearly.

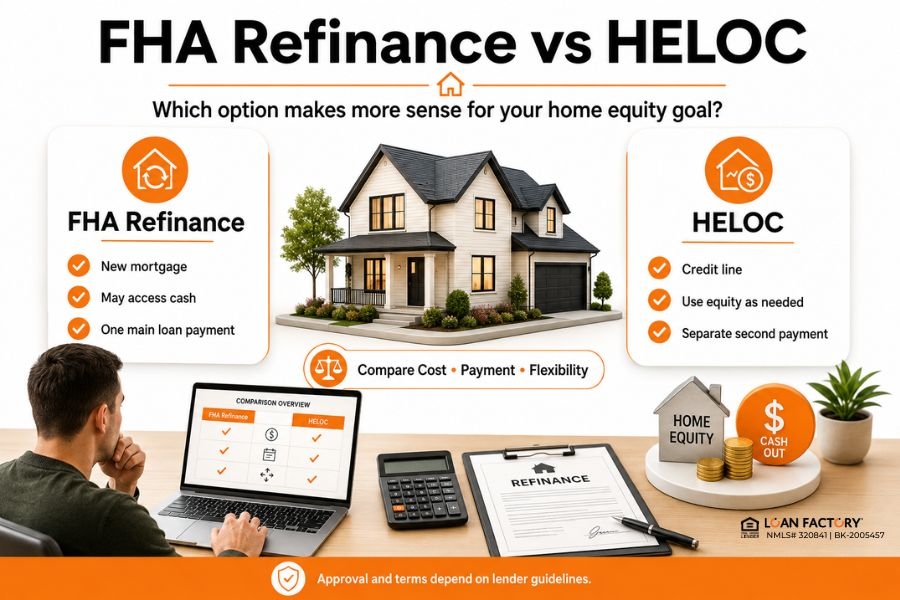

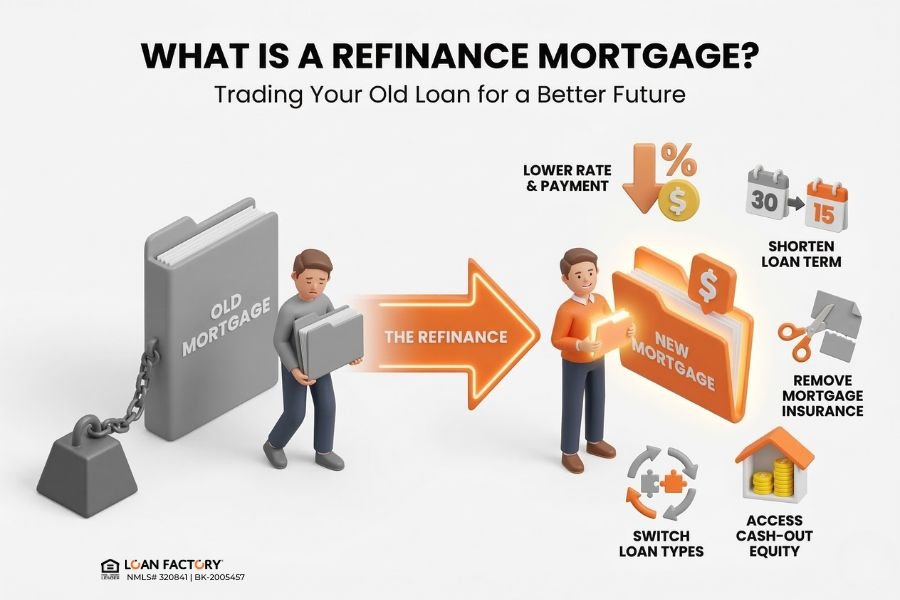

What Is an FHA Refinance? An FHA refinance replaces your existing loan with another FHA loan.

Common FHA refinance options include:

FHA Streamline Refinance FHA Rate-and-Term Refinance FHA Cash-Out Refinance FHA refinancing is often chosen for:

Simpler qualification More flexible credit standards Borrowers with limited equity However, FHA loans require mortgage insurance.

If you’re unsure how FHA mortgage insurance works, review our full guide on FHA mortgage insurance explained.

What Is a Conventional Refinance? A conventional refinance replaces your loan with a conventional mortgage.

Homeowners often choose this option to:

Remove FHA mortgage insurance (MIP) Gain long-term flexibility Access credit-based pricing advantages Avoid lifetime insurance costs If your primary goal is removing FHA insurance, see our breakdown of how much equity you need to remove FHA MIP.

Feature

FHA Refinance

Conventional Refinance

Mortgage Insurance Required (MIP) PMI only if under 20% equity Insurance Removal Often lifetime May be removed at 80% LTV Credit Flexibility More flexible More credit-based pricing Appraisal Requirement Often required (except Streamline) Usually required Long-Term Flexibility Limited Greater Best For Lower credit / low equity Improved credit / higher equity

Actual benefits depend on loan structure, credit profile, and long-term plans.

When FHA Refinance May Be Better An FHA refinance may make more sense if:

Your credit score is still rebuilding You have limited equity You want simplified documentation (FHA Streamline) You do not qualify for competitive conventional pricing FHA Streamline , for example, may reduce paperwork — but it does not eliminate mortgage insurance.

See our full guide on FHA Streamline refinance pros and cons for deeper analysis.

→ Read more: Can You Refinance FHA With Less Than 20% Equity?

When Conventional Refinance May Be Better A conventional refinance may be stronger if:

You have close to or over 20% equity Your credit score has improved You want to remove mortgage insurance You plan to stay in the home long term You want more flexibility later In many real-world refinance cases, homeowners switched from FHA to conventional primarily to eliminate lifetime MIP — not because of rate changes alone.

If you're evaluating timing, read our guide on does refinancing lower your monthly payment

Mortgage Insurance: The Biggest Difference The most significant difference between FHA and conventional refinancing is how mortgage insurance behaves.

FHA MIP Required on all FHA loans Often lasts for life of the loan if down payment was under 10% Not credit-based Conventional PMI Required only under 20% equity May be removed once sufficient equity is reached Credit-based pricing This difference alone can impact long-term cost significantly.

Which One Is Better in 2026? There is no universal answer.

The better option depends on:

Your current loan balance Estimated home value Credit score Break-even timeline Insurance cost comparison If you're unsure how to calculate refinance timing, review our guide on how to calculate your refinance break-even point.

Sometimes waiting improves your outcome more than refinancing immediately.

A Strategic Way to Decide Instead of asking:

“Which loan type is better?”

Ask:

Does switching eliminate long-term insurance cost? Does my improved credit qualify me for better pricing? Will I stay in the home long enough to benefit? Does the refinance improve flexibility? A structured comparison across lenders is key.

Why Homeowners Compare FHA vs Conventional Refinance with Loan Factory Choosing the right refinance structure requires transparent comparison — not guesswork.

Why Homeowners Choose Loan Factory:

Zero application or junk fees Transparent side-by-side comparison of 240+ wholesale lenders Local loan advisors focused on total loan cost — not just interest rate AI-powered MOSO platform for real-time pricing and scenario analysis Trusted guidance led by Thuan Nguyen, #1 Loan Officer in the U.S. We help you compare FHA and conventional structures side-by-side so you can make an informed decision.

Sometimes FHA is the better choice.

Our role is to show you the difference clearly.

Ready to Compare FHA vs Conventional Refinance Options? Apply online: https://www.LoanFactory.com/apply https://www.LoanFactory.com/quote www.loanfactory.com/mortgage-rate-alert

Based on real-world jumbo loan scenarios reviewed by Loan Factory’s lending team across multiple high-cost markets.

This content is for informational purposes only and not a commitment to lend. Loan options, rates, and terms depend on credit, income, property value, underwriting, and investor guidelines.

FAQ: FHA vs Conventional Refinance