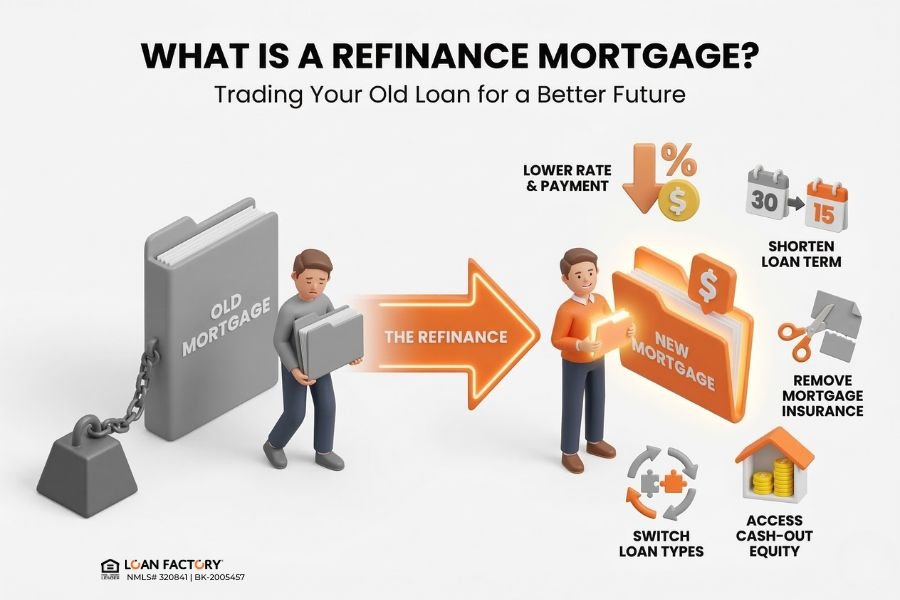

A refinance may make sense when the new loan gives you a clear benefit: a lower payment, lower total interest, shorter loan term, access to home equity, removal of mortgage insurance, or a more stable loan structure.

But the right time to refinance is not based on the interest rate alone. You should also compare closing costs, break-even point, loan term, mortgage insurance, and how long you plan to keep the home.

Use the table below as a quick starting point.

Industry Insight: Refinance Is Becoming More Strategic In a Mortgage Professional America article, Thuan Nguyen, CEO of Loan Factory, explained that refinance has not disappeared — it has become more strategic. Instead of simply waiting for rates to drop, homeowners and mortgage professionals now rely more on technology, pricing transparency, rate alerts, and proactive loan reviews.

That matters because many refinance opportunities are easy to miss. A rate change, home equity increase, mortgage insurance update, improved credit profile, or cash-out need could all create a reason to compare options.

Read the original MPA article here: How technology is reshaping the refinance opportunity for brokers

Your Situation

Why Refinancing May Help

What to Check First

Current rates are lower than your existing rate You may be able to reduce your monthly payment or interest cost Closing costs and break-even point Your credit score or income improved You may qualify for better pricing or loan terms Updated credit, income, and debt profile You have FHA mortgage insurance Refinancing into a conventional loan may help remove monthly mortgage insurance if you have enough equity Home value, loan-to-value ratio, and lender guidelines You want to pay off your loan faster A shorter term may reduce total interest paid Monthly payment comfort and long-term budget You need cash for a major purpose A cash-out refinance may allow access to home equity New loan amount, equity, rate, and total cost You have an adjustable-rate mortgage Refinancing into a fixed-rate loan may create more payment stability Current ARM terms and fixed-rate options You want to compare lenders Different lenders may price the same refinance differently Rate, fees, credits, mortgage insurance, and APR

The Best Time to Refinance Is When the Math Works A refinance should usually answer one important question:

Will the benefit be greater than the cost?

For example, if refinancing saves you money each month but costs several thousand dollars to complete, you need to know how long it will take to recover those costs.

This is called your refinance break-even point.

How to Calculate Your Refinance Break-Even Point Use this simple formula:

Refinance closing costs ÷ monthly savings = break-even months

Example:

Refinance Cost

Estimated Monthly Savings

Break-Even Point

$4,000 $200/month 20 months $5,000 $250/month 20 months $6,000 $150/month 40 months

In simple terms, if you plan to keep the home or loan longer than the break-even period, refinancing may be worth reviewing. If you plan to sell soon, refinance costs may outweigh the benefit.

That is why a good refinance review should not stop at the interest rate. It should include:

Monthly payment difference Closing costs Lender credits or discount points APR Mortgage insurance changes Loan term Total interest over time Cash-out amount, if applicable How long you expect to keep the loan → Read more: what happens when you refinance your home

7 Signs It May Be Time to Refinance Your Mortgage 1. Mortgage Rates Are Lower Than Your Current Rate This is the most common reason homeowners consider refinancing.

But you do not always need a dramatic rate drop for refinancing to matter. Even a smaller rate improvement may help if your loan balance is large, your current rate is high, or your refinance costs are low.

The better question is:

Does the new loan create enough savings or value after costs?

A refinance may be worth comparing if you can lower your payment, reduce total interest, or improve your loan structure without creating unnecessary costs.

2. You Can Lower Your Monthly Payment Many homeowners refinance to reduce their monthly mortgage payment.

This can help improve monthly cash flow, especially if household expenses have increased. However, lowering your payment can sometimes extend your loan term, which may increase total interest over time.

Before choosing this option, compare:

Option

Monthly Payment

Total Interest

Best For

Lower rate, same remaining term May reduce payment and interest Often more efficient Borrowers focused on savings Lower rate, new 30-year term May create larger payment relief Could increase long-term interest Borrowers needing cash flow Shorter term refinance May increase payment Could reduce total interest Borrowers wanting faster payoff

The right choice depends on your budget and long-term plan.

3. You Want to Remove Mortgage Insurance If you bought your home with a low down payment, you may be paying monthly mortgage insurance.

For FHA loans, mortgage insurance can stay for a long time depending on your original loan terms. If your home value has increased or you have paid down your loan, refinancing into a conventional loan may help remove monthly mortgage insurance, depending on your equity and lender guidelines.

This is one of the most overlooked refinance opportunities because the savings may come from removing mortgage insurance, not only from lowering the interest rate.

4. Your Credit Score or Financial Profile Improved If your credit score, income, savings, or debt-to-income ratio has improved since you first got your mortgage, you may qualify for a better refinance structure.

Lenders typically review:

Credit score Income stability Debt-to-income ratio Home equity Property type Loan purpose Occupancy Loan amount Mortgage payment history A borrower who was approved under one set of conditions two or three years ago may have stronger options today.

5. You Want to Switch From an ARM to a Fixed-Rate Mortgage If you have an adjustable-rate mortgage, your payment may change after the fixed period ends.

Refinancing into a fixed-rate mortgage may make sense if you want more predictable monthly payments and plan to keep the property long term.

This is especially important if:

Your ARM adjustment period is approaching Your payment could increase You prefer long-term stability You do not want to monitor future rate changes A fixed-rate refinance may not always produce the lowest starting payment, but it can create more certainty.

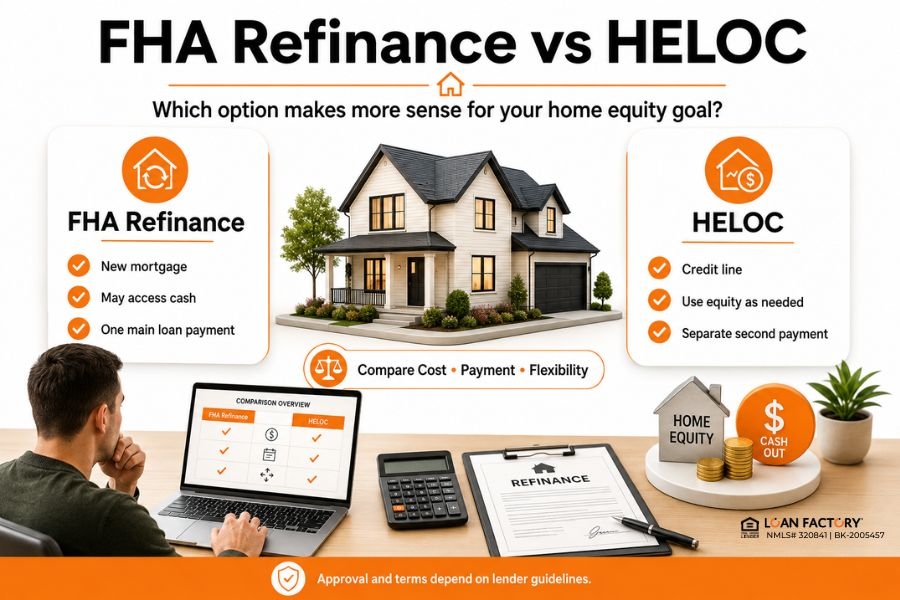

6. You Need Cash From Home Equity A cash-out refinance allows you to replace your current mortgage with a larger loan and receive part of your home equity as cash.

Homeowners may consider this for:

Home improvements Debt consolidation Investment property planning Emergency reserves Education expenses Major life events A cash-out refinance should be reviewed carefully because it increases your loan balance and may change your rate, payment, and long-term interest cost.

It may be a useful tool, but it should be compared against alternatives such as a HELOC, home equity loan, or keeping your current mortgage.

→ Read more: FHA Refinance vs HELOC : Which Makes More Sense?

7. You Have Not Compared Your Loan in a While Many homeowners assume their current mortgage is still the best option because they have not reviewed it recently.

But mortgage pricing changes often. Lender guidelines change. Home values change. Your credit profile may change. Loan programs may also change.

This is why technology and rate alerts matter.

Homeowners should not have to monitor mortgage rates every day. A smart refinance strategy uses technology to watch for opportunities and compare the numbers when the timing may make sense.

Why Rate Alerts Matter for Refinancing One of the biggest mistakes homeowners make is waiting until they “hear rates are low” before checking refinance options.

By then, pricing may have already changed, lenders may be busier, or another lender may have already reached out with an offer.

A mortgage rate alert can help you stay informed when market movement may create a reason to review your loan. Instead of guessing, you can compare your current mortgage against available options and decide based on real numbers.

A rate alert is especially useful if:

You bought or refinanced when rates were higher You want to refinance but are waiting for better timing You are close to removing mortgage insurance Your home value has increased You want to monitor cash-out refinance options You want to compare multiple lenders before deciding The goal is not to refinance every time rates move. The goal is to know when the numbers are worth reviewing.

That is the same idea Thuan Nguyen highlighted in Mortgage Professional America: refinance is no longer only about waiting for the perfect market. It is about being prepared to act when the right opportunity appears.

Mortgage Broker vs Bank: Why It Matters for Refinance When you refinance with a single bank or retail lender, you usually see that lender’s products, pricing, and guidelines.

A mortgage broker can compare options from multiple wholesale lenders. This can be helpful because refinance decisions depend on more than the interest rate.

Different lenders may vary on:

Interest rate Lender fees Discount points Lender credits Mortgage insurance pricing Appraisal requirements Cash-out rules Debt-to-income limits Credit score overlays Turn times If one lender does not fit your scenario, a broker may be able to compare another lender without forcing you to restart the entire process.

This flexibility can be especially valuable when your refinance includes cash-out, mortgage insurance removal, self-employment income, investment property, or a more complex loan structure.

When Refinancing May Not Make Sense Refinancing is not always the right move.

You may want to wait or compare more carefully if:

You plan to sell the home soon The break-even period is too long Closing costs are too high The new payment is not meaningfully better You would restart your loan term without enough benefit Your credit score has dropped Your home equity is too low You already have a very strong rate You are only focused on monthly payment and not total cost A refinance should support your financial goal. It should not be done only because a lender is advertising a lower rate.

→ Read more: No-Closing-Cost Refinance | Lower Your Rate Without Upfront Costs

What Documents Do You Need to Review a Refinance? To compare refinance options, you may need:

Current mortgage statement Homeowners insurance information Recent pay stubs or income documents W-2s or tax returns, depending on income type Bank statements Current property value estimate Information about property taxes and HOA dues Current loan type and interest rate Payoff estimate, if available If you are self-employed, own investment property, or want a cash-out refinance, additional documentation may be needed.

How Loan Factory Helps You Compare Refinance Options Once you understand when refinancing may make sense, the next step is not to guess. The next step is to compare.

Loan Factory helps borrowers review refinance options across a wide lender network, using technology and side-by-side pricing to help identify loan structures that may fit the borrower’s goals.

Why Choose Loan Factory for Mortgage Refinance? Loan Factory is built for borrowers who want more transparency, more comparison, and a clearer refinance decision.

Here is how Loan Factory can help:

Compare 240+ lenders: Instead of relying on one bank’s pricing, Loan Factory helps compare options across a broad wholesale lender network. Tera AI-powered technology: Loan Factory’s mortgage platform helps support faster pricing, borrower communication, and loan review. Rate alert support: Borrowers can monitor refinance opportunities instead of trying to watch the market alone. Side-by-side pricing: Compare rate, fees, credits, and mortgage insurance so you can focus on the full cost, not just the advertised rate. Zero application or junk fees: Loan Factory focuses on a lower-cost mortgage experience. Local loan advisors: Get guidance from licensed mortgage professionals who can review your scenario. The refinance decision should be based on real numbers. Loan Factory’s role is to help you compare those numbers clearly before you decide.

Ready to See If Refinancing Makes Sense? You do not need to wait until rates drop dramatically. If your current loan, home value, credit profile, or financial goals have changed, it may be worth comparing your options now.

Apply online: https://www.LoanFactory.com/apply https://www.LoanFactory.com/quote www.loanfactory.com/mortgage-rate-alert

Experience note: This article is based on real refinance scenarios reviewed by Loan Factory’s lending team, including rate-and-term refinances, cash-out refinances, mortgage insurance removal reviews, and borrower rate alert opportunities across multiple U.S. markets.

Disclaimer: This content is for educational purposes only and is not a commitment to lend. Refinance eligibility, rates, fees, savings, mortgage insurance, cash-out limits, and loan terms depend on credit profile, property type, loan amount, equity, underwriting review, investor guidelines, and market conditions. Terms & Conditions apply to the Loan Factory $2,000 Best Price Guarantee.

FAQ: When Should I Refinance My Mortgage?