Becoming a Mortgage Loan Originator (MLO) is often described as either “easy money” or “too complicated.”

Both are misleading.

People enter the mortgage industry from many different backgrounds, but long-term success depends less on prior experience and more on understanding how the job actually works—especially its process, compliance, and commission-based income structure.

This guide explains how people become mortgage loan originators , what the early stages really look like, and how income is built over time—based on how the career actually works.

What Does a Mortgage Loan Originator Actually Do? A Mortgage Loan Originator is responsible for guiding borrowers through the loan process, not approving loans or making credit decisions.

In practice, an MLO:

Communicates with homebuyers or homeowners Collects financial and property information Explains available loan options (without guaranteeing approval) Submits loan applications Works with processors and underwriters to close loans The role combines communication, process management, and compliance.

Strong finance or tech skills can help—but they are not the only path to success.

→ Read more: Mortgage Loan Originator Salary in the US

Do You Need Strong Finance or Technology Skills to Become an MLO? Some aspiring MLOs already understand finance or are comfortable with technology.

Both can succeed.

If you have a finance background, you may grasp guidelines faster If you’re comfortable with technology, you may adapt to systems more easily If you’re newer to both, modern tools and structured training are designed to support learning What consistently matters most is:

Following a defined process Communicating clearly with borrowers Submitting accurate files Learning from feedback Mortgage origination rewards execution and consistency, not just technical knowledge.

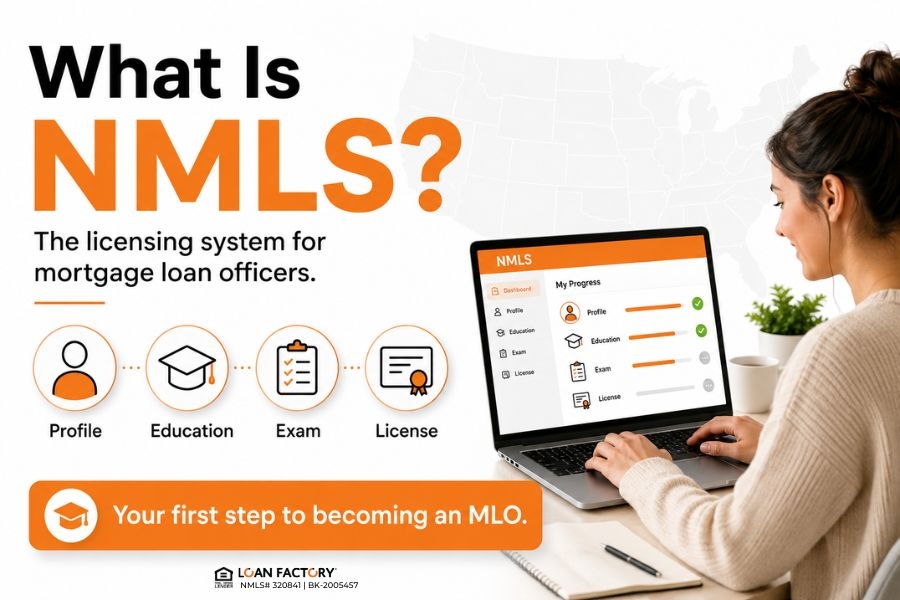

How to Become a Mortgage Loan Originator In the U.S., the process typically includes:

Completing required NMLS pre-licensing education Passing the SAFE Mortgage Loan Originator exam Applying for state licensing through NMLS Joining a licensed mortgage company These steps are the same regardless of background.

→ Read more: How to Pass the SAFE MLO Exam on Your First Try?

How People Move Through This Process Efficiently People progress more smoothly when they:

Choose one education path and complete it with focus Prepare intentionally for the SAFE exam Join a company that provides clear onboarding and compliance guidance Efficiency comes from clarity—not rushing or skipping steps.

How Mortgage Loan Originators Get Paid Most mortgage loan originators:

Are commission-based Earn income only when loans close and fund Do not receive guaranteed monthly income This applies to both:

W2 Loan Officers 1099 Loan Officers Practical Example A borrower completes a loan and it closes The brokerage receives payment from the lender The loan officer earns commission based on the agreed structure If a loan does not close, no commission is earned.

Understanding this early helps set realistic expectations and supports long-term planning.

What “Building Higher Income” Really Means in Mortgage Higher income in mortgage origination usually comes from:

Closing loans consistently Reducing errors and rework Managing pipelines effectively Building repeat and referral business It is less about:

Chasing the highest commission percentage Switching companies frequently Looking for guarantees → Read more: how to be a successful mortgage loan officer?

Simple Comparison Two loan officers may work in the same market with similar tools:

One submits clean, complete files → more closings One submits inconsistent files → more fallouts Over time, the first officer typically builds more stable income, regardless of background.

Is This Career a Good Fit for You? This career often fits individuals who:

Are comfortable with performance-based income Can communicate clearly with clients Are willing to learn guidelines and compliance Prefer building skills over time It may not fit those who:

Require a fixed paycheck every month Dislike sales or client interaction Prefer minimal regulatory oversight Expect quick results without a learning curve Being honest about this helps avoid frustration later.

1099 vs W2: How to Think About It You’ll hear both terms frequently.

W2 Loan Officers are employees, paid through payroll, with taxes withheld 1099 Loan Officers are independent contractors, responsible for their own taxes Both are typically commission-based. Neither model guarantees income.

Many loan officers choose different models at different stages of their careers.

What the First Few Months Often Look Like While timelines vary, many new loan officers experience:

Initial training and system onboarding Learning guidelines and documentation Submitting early applications First closings occurring after a learning period Some progress faster, some slower. There is no universal timeline—and that is normal.

Especially early on, the brokerage you choose can affect:

How clearly compensation is explained How much support is available How efficiently you learn systems and compliance How smoothly loans move through the process The platform doesn’t guarantee success—but it can reduce unnecessary obstacles.

→ Read more: Best Mortgage Companies to Work For as a Loan Officer in the U.S.

Why Many Loan Officers Choose Loan Factory Loan Factory is built to support loan officers at different experience levels—within a transparent, compliant, and performance-based brokerage structure.

What Loan Factory Offers Loan Officers: Both W2 Outside Salesperson and 1099 Independent Contractor models Clear commission structures on closed and funded loans 100% commission on eligible self-generated loans, minus a flat $595 fee per file No desk fees or junk fees Free MOSO platform (CRM, LOS, pricing, marketing, compliance tools)Access to 240+ wholesale lenders In-house underwriting support and $500 processing per file Company-generated lead programs (with disclosed splits) Mentorship from Thuan Nguyen (#1 Loan Officer in the U.S.) Weekly training sessions and Loan Factory Academy Compensation is paid only on closed and funded loans and may be subject to early payoff and compliance review.

Not Licensed Yet? If you’re still in the early stage and don’t have your mortgage loan originator license yet, you don’t need to figure everything out on your own.

Loan Factory provides a clear, step-by-step overview of how to become a licensed loan officer in the U.S., including:

Required education Licensing exams Onboarding and next steps Learn more here: https://www.loanfactory.com/becoming-a-loan-officer

Already Licensed or Exploring Your Next Move? If you already have your license—or want to learn how loan officers structure their careers, compensation, and growth within a compliant brokerage model:

Join the Loan Factory webinar: https://www.loanfactory.com/loan-officer

Or call 714-591-8143 to speak with our team.

Disclaimer This article is for informational purposes only and does not constitute an offer of employment, compensation guarantee, or commitment to lend.

FAQ