Key Takeaways It’s a Career of Guidance: Being a Mortgage Loan Officer means you're a trusted advisor helping people achieve the dream of owning a home.Licensing is a Must: You'll need to complete 20 hours of NMLS pre-licensing education, pass the SAFE exam, and get licensed in your state under a sponsoring lender.No Experience? Start in a Support Role: The smartest way in for a newcomer is to work as a Loan Officer Assistant or Processor. You'll gain priceless experience while earning a salary.Success is Strategic: You can get past the early hurdles by picking a tech-focused employer, finding a specific niche, getting a mentor, and being an amazing communicator.Technology is Your Friend: Use automation to cut down on paperwork, work more efficiently, and give modern borrowers the fast, transparent experience they expect.Are you thinking about how to become a mortgage loan officer in 2025? It’s one of those rare jobs where you get to be the person who hands over the keys to a life-changing dream—helping people finally own their own homes. But let’s be real: looking in from the outside, the whole thing can seem incredibly complicated. You’ve got licensing exams, a ton of industry jargon, and that one big question looming over it all: "How in the world am I supposed to make a living on commission?"

This guide is that map. We’re going to walk through every step, tackle those tough questions head-on, and give you a real, actionable game plan to build a career as a Mortgage Loan Officer (MLO) that’s not just profitable, but genuinely fulfilling—even if you’re starting from square one.

→ Read more: What is the highest salary for a mortgage loan officer?

Overview: What Does It Take to Become a Mortgage Loan Officer? Before we get into the "how-to," let's talk about the "what." Getting a true feel for the role is the best way to know if it’s really for you.

What Is a Mortgage Loan Officer? A Mortgage Loan Officer is so much more than a numbers person or a sales rep. Think of yourself as a guide, a strategist, and the person your clients trust with one of the biggest financial decisions of their lives. Your main job is to help people navigate the world of home financing. That means sitting down with them, getting a clear picture of their financial health, explaining their loan options in plain English, and holding their hand through the entire application and approval maze.

You're the human touch in a process that can feel cold and robotic. You’re the steady voice that calms a nervous first-time homebuyer and the creative problem-solver who finds a way to get a tricky loan over the finish line.

Day-to-Day Duties of a Loan Officer If you're picturing a quiet 9-to-5 desk job, you might want to adjust that image. Life as an MLO is dynamic, and you wear a lot of different hats every single day. A typical day might have you:

Generating Leads & Networking: You’re always building connections. This means grabbing coffee with real estate agents, touching base with financial planners, and being an active part of your community. This is what keeps your business running.Client Consultation & Analysis: This is where you sit down with potential borrowers to really listen. You’ll dig into their financial situation, their long-term goals, and their credit history to figure out the absolute best mortgage for them.Application Management: You’ll guide clients through the loan application, making sure every single piece of paper is correct and accounted for. Yes, this is where the infamous paperwork lives, but the smart MLOs today have some slick tech to make it manageable.Collaboration & Problem-Solving: You're the central hub of communication. You’ll work hand-in-hand with underwriters (who give the final loan approval), processors (who put the file together), and appraisers (who determine the home's value) to keep everything moving smoothly.It's easy to feel like you’re being pulled in a million directions at once, and it can definitely burn out newcomers. But if you get your systems down and have the right mindset, it’s a thrilling challenge where no two days ever feel the same.

→ Read more: What Does a Loan Officer Do? Career Overview & Day-to-Day Duties

How to Become a Loan Officer: Your Step-by-Step Guide Ready to jump in? Here’s the nitty-gritty on how to become a legally licensed Mortgage Loan Officer in the United States.

Basic Requirements to Become a Loan Officer Before you can even crack open a textbook, you need to check a few boxes:

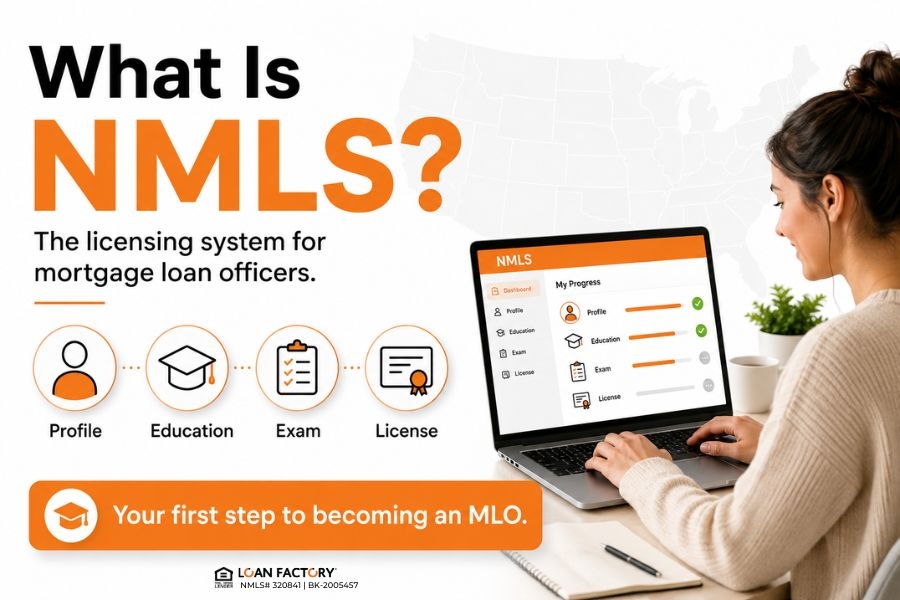

You have to be at least 18 years old. A high school diploma or GED is a must. You’ll need to pass a criminal background check and a credit check. After all, this career is built on a foundation of trust, integrity, and financial responsibility. Educational Background & Certifications The first big step on your official journey is required by a piece of federal law called the SAFE Act. Every single person who wants to be an MLO has to:

Complete 20 hours of NMLS Pre-Licensing Education: This is a course approved by the Nationwide Multistate Licensing System & Registry (NMLS) . It covers the essentials: federal laws, ethics, how to spot fraud, and the basics of lending.Pass the SAFE MLO Test: This national exam quizzes you on everything you learned in your course. A passing score of 75% or higher is required.While having a college degree in something like finance or business is great, it’s not required. Your NMLS certification is the real ticket to get in the door.

Once you’ve passed that SAFE exam, you’ll need to get a state license for every state where you plan to do business.

State-Specific Requirements: On top of the national requirements, many states have their own courses you’ll need to take to learn their specific laws.Sponsorship: Here’s a key detail: you don't get your license in a vacuum. You have to be hired by a licensed mortgage lender—like a bank, credit union, or mortgage brokerage—who will "sponsor" your NMLS license application.Continuing Education (CE): This isn't a one-and-done deal. To maintain an active license, 8 hours of NMLS-approved continuing education must be completed annually.This all might seem like a lot of red tape, but it’s there to protect consumers. Think of it as the framework that gives you your professional credibility.

→ Read more: Is It Hard to Make It as a Loan Officer? Tips Inside

Becoming a Loan Officer With No Experience This is the question I get more than any other: "I’ve been a teacher/a retail manager/I just graduated—how can I possibly break into a field like this?" It's much simpler than you imagine. Some companies are indeed hesitant to hire rookies, but with the right strategy, you can turn your fresh perspective into your greatest strength.

How to Start in the Industry Without a Background Here's the secret: don't try to become a Loan Officer on day one. Instead, work your way in from a different angle. This method alleviates the initial "commission-only" strain, offering a consistent salary as you gain experience. It also solves the problem of not having a mentor by putting you right in the middle of the action.

Entry-Level Loan Officer Jobs & Internships The absolute best way to become a loan officer when you have no experience is to first become a Loan Officer Assistant (LOA) or a Processor.

Loan Officer Assistant (LOA): Think of this as your apprenticeship. You'll work right alongside a seasoned MLO or a whole team of them. You’ll learn exactly how to structure a loan, what underwriters are really looking for, and how to talk to clients.Mortgage Processor: Processors are the people who make sure every piece of documentation is in the loan file before it goes to the underwriter. In this role, you’ll become a master of the paperwork side of things, which will make you a far more effective MLO down the road.These positions offer valuable on-the-job training and a steady income while you prepare for your NMLS exam.

Networking & Learning Opportunities for Beginners While you're working in one of those support roles, start laying the groundwork for your future business:

Partner with New Realtors: Don't go chasing the top-producing agents in your town right away. Instead, find real estate agents who are just getting started, too. You can learn the business and grow your careers together, building a loyal partnership that could last for years.Share Your Journey Online: Start a professional-looking social media account where you document what you're learning about the mortgage world. You don’t have to pretend you're an expert. Just be authentic. It builds trust and establishes your personal brand before you even have a single client.Attend Local Industry Events: Show up at events hosted by local real estate boards or mortgage associations. Your only job is to listen, learn, and introduce yourself.→ Read more: How Much Mortgage Loan Officers Make Per Loan?

Common Challenges When Becoming a Loan Officer A career as an MLO is incredibly rewarding, but let's be honest—it isn't easy. To overcome future challenges, you must first understand what they are.

Is Becoming a Loan Officer Difficult? Yes, it can be. New MLOs frequently encounter significant obstacles, including:

Unstable Income: Most MLOs are paid 100% by commission. It can easily take 6 to 12 months to get a steady stream of clients going. Ensure you have at least six months of living expenses saved to cover your costs.Tough Competition: It's a crowded field. When you don't have a long list of past clients, building trust with new ones and with realtors can be a slow process. First-time homebuyers especially tend to lean towards officers with more experience.The Technology & Paperwork Overload: If you're new, it's easy to spend half your day just chasing down documents. This can lead to mistakes, slow down the loan process, and cause a lot of stress.But here’s the good news: every single one of these challenges can be managed with the right game plan.

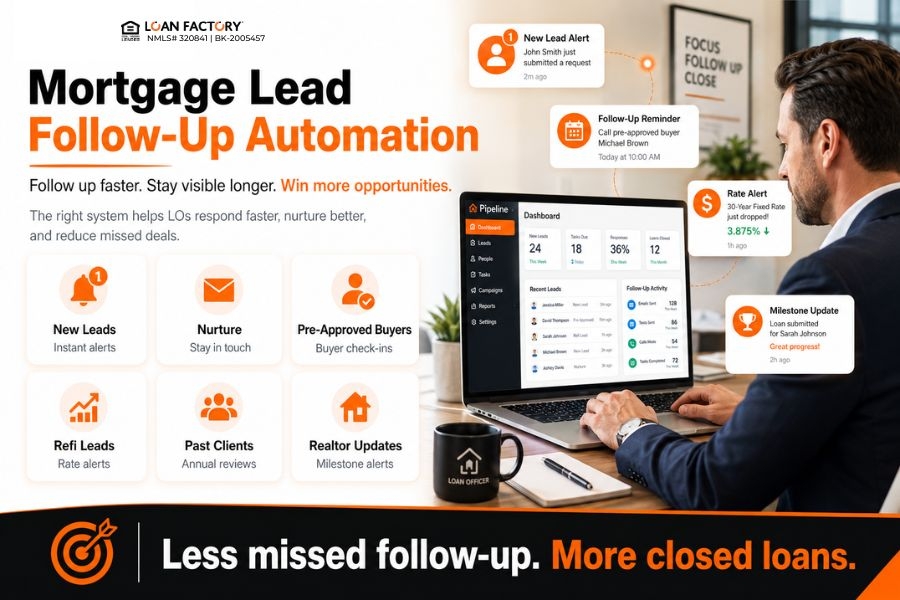

Tips for Succeeding Early in Your Career Choose the Right Employer: Don't just chase the company offering the highest commission split. Your first boss matters. A lot. Look for a tech-savvy lender that gives you modern tools (like a digital portal for borrowers) and has a solid training or mentorship program. This simple solution can prevent many initial problems.Let Technology Do the Boring Stuff: Your most valuable time is spent building relationships and talking to clients. Administrative tasks are what drains your energy. Use tools for eSignatures, automated income and asset checks, and a good Customer Relationship Management (CRM) system to handle the busy work. Today's clients expect a smooth, digital process, and the right tech helps you give them one.Find a Niche: Don't try to be the loan officer for everyone. Cultivate expertise within a niche demographic. You could specialize in VA Loans for veterans, FHA loans for first-time buyers, or loans for self-employed people. There’s truth to the saying, "The riches are in the niches." Expertise builds trust faster than anything.Seek out a veteran MLO who is willing to show you the ropes: A good mentor can help you figure out complex loan situations, steer you away from common rookie mistakes, and give you the encouragement you need to get through those tough first few months.Master Communication: Think about it from the buyer's point of view: they are stressed and making the biggest purchase of their lives. They crave information. Be crystal clear about what to expect from the start, give them regular updates (even if it's just to say you're still working on it), and be available to answer their questions. Amazing service is your best marketing tool, and it's the fastest way to get people to refer their friends and family to you.Why should you join our team at Loan Factory? Throughout this guide, we’ve talked about how crucial the right environment is for your success. We emphasized choosing a tech-forward employer with strong support because, frankly, your brokerage can either hold you back or launch you forward.

At Loan Factory, we built our company around launching MLOs forward. We live by the principles of working smarter, which is why we invested millions into a proprietary technology platform that automates the administrative tasks that drain your day. This means less time chasing paperwork and more time doing what matters: building relationships and guiding clients. Our seamless digital experience gives your borrowers the speed and transparency they expect, making you the trusted expert from the very first click.

A great career isn't just about tech; it's about people. Our team is built on a culture of collaboration and growth, not cutthroat competition. Whether you're a seasoned pro or a brand-new MLO hungry to build your business, you will find the support, mentorship, and resources here to build a career on your terms.

Ready to define your success story? Apply today at www.loanfactory.com/en/loan-officer Or call us at (714) 591-8143 to explore your future.

Frequently Asked Questions (FAQs)