If you're asking “can I be a mortgage loan officer and a realtor at the same time?”, the answer is:

Yes — you can do both, and it’s one of the fastest ways for Realtors to increase income and control more of the client experience.

Here’s everything you need to know.

Can You Be Both a Realtor and a Mortgage Loan Officer? Yes. Most states allow dual licensing, and thousands of real estate agents already do both successfully.

For many professionals, adding mortgage is a natural extension because:

You already understand the homebuying process You already have leads Clients already trust you You become a more complete advisor How Much Can You Earn as Both a Realtor and a Loan Officer? Loan officers typically earn 1%–1.5% of the loan amount.

Example: $500,000 loan → $5,000–$7,500 per file.

1. With Loan Factory You keep 100% commission, paying only $595 per file.

2. Combined Income If you close:

1 loan/month → +$4,500–$7,000 extra 2 loans/month → +$9,000–$14,000 extra 3 loans/month → +$13,500–$21,000 extra This is in addition to your Realtor commissions.

What You Actually Do as BOTH a Realtor and a Loan Officer 1. Guide clients on homes & financing You explain:

What they can afford Loan programs Monthly payment estimates How financing affects offers 2. Show homes & write offers (Realtor role) Your core real estate duties stay the same:

Finding homes Tours Offers Negotiation 3. Pre-approve clients & run pricing (Loan Officer role) You can:

Issue pre-approvals Compare lenders Run loan scenarios Strengthen offers 4. Coordinate the full transaction smoothly Clients now deal with one trusted expert from:

Pre-approval → House hunting → Offer → Loan → Closing This dramatically increases customer satisfaction and referral flow.

5. Build two income streams from the same client base Your existing buyers become mortgage clients — your loan clients become real estate clients.

It’s the most efficient form of business growth.

Good news: Realtors have a huge head start. Here’s the simple path:

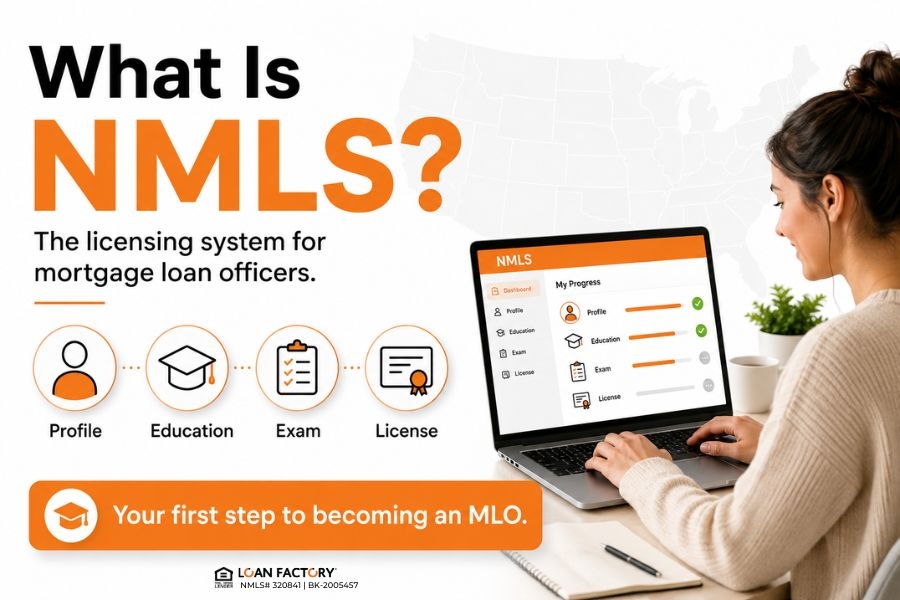

Step 1 — Complete the 20-hour NMLS course Online, self-paced, usually 3–7 days.

→ Read more: Who is required to have an NMLS number?

Step 2 — Pass the SAFE MLO exam Loan Factory provides study resources and guidance.

→ Read more: How to Pass the SAFE MLO Exam on Your First Try

Step 3 — Apply for your state LO license Submit fingerprints, background check, and application.

Step 4 — Join a mortgage company This gives you:

Lender access Pricing engine LOS + CRM Compliance Underwriting Training Step 5 — Start originating loans Once you’re licensed and sponsored, you can start working on live files.

The entire process can be completed in a few weeks.

→ Read more: How to become a mortgage loan originator with no experience?

How to Manage Both Jobs Successfully Realtors often worry about juggling two roles — but in reality, it’s simpler than it sounds.

Here’s how successful dual-licensed agents manage both:

1. Pick a primary focus (usually real estate) Most agents stay focused on real estate and add mortgage as:

an additional income stream, a value-added service, and a tool to qualify clients faster. 2. Use mortgage mainly for your own buyers You don’t have to market yourself as a full-time LO.

You just serve:

buyers you already have referrals from past clients warm leads you’re already nurturing This keeps workload manageable.

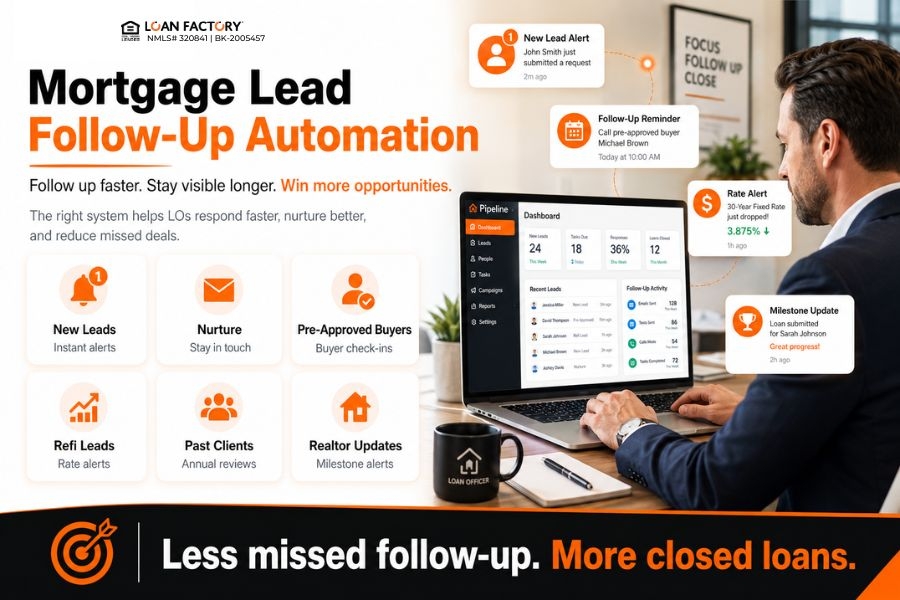

3. Use technology to automate the loan process Loan Factory’s MOSO platform handles:

Disclosures pricing document collection updates communication This reduces time spent on the mortgage side by 70%+.

4. Let underwriters and processors do the heavy lifting Your job is client communication, not paperwork.

underwriting processing conditions verifications You stay in your zone of strength: relationships.

→ Read more: Loan Officer vs Underwriter: Who Does What?

5. Create a weekly workflow Most dual agents follow a simple rhythm:

Morning: mortgage updates & pricing Daytime: show homes, write offers Evening: follow-ups, lead nurturing No need to “switch hats” constantly — both jobs support each other.

Why Real Estate Agents Choose Loan Factory When Becoming Loan Officers Loan Factory gives Realtors the ideal platform to succeed as Loan Officers:

100% commission (flat $595 per file) No splits. No desk fees.

CRM, LOS, pricing, marketing, compliance — saving ~$963/month.

Access to 240+ wholesale lenders Offer buyers the best pricing available.

In-house underwriting + $500 processing Company-generated leads in 42 states Mentorship from Thuan Nguyen (#1 LO in the U.S.) Weekly training + Loan Factory Academy This combination makes Loan Factory the most profitable and simplest path for Realtors to expand into mortgage.

Ready to Grow Your Career? Join the Loan Factory webinar: https://www.loanfactory.com/loan-officer

Call for details: 714-591-8143

FAQ: Can I Be a Mortgage Loan Officer and a Realtor?